Stock Markets

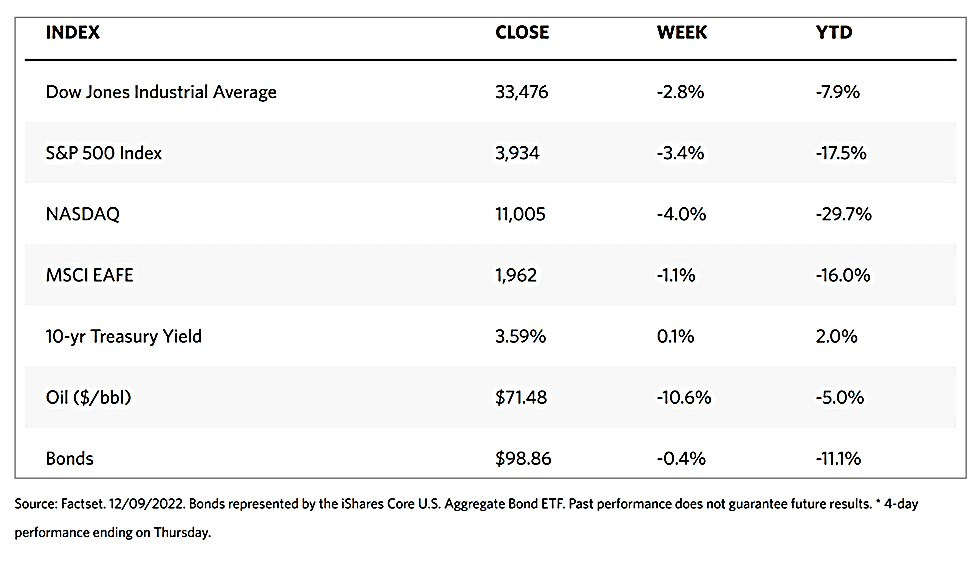

In the week just ended, stocks fell for all major indexes, halting the rally that began in mid-October. Ironically, the current pessimism hinges on the perception of coming economic weakness driven by evidence of ongoing economic strength in the economy itself. These data consist of elevated wage gains, robust job growth, and resilient consumer spending trends, all leading to the likelihood that the Federal Reserve’s attempts to control inflation are not likely to slow down. The economy will likely decline as collateral damage from continuing aggressive rate hikes. The Dow Jones Industrial Average (DJIA) lost 2.77% and the Dow Jones Total Stock Market Index fell by 3,60%. The S&P 500 Index descended 3.37%, while the Nasdaq Stock Market Composite declined 3.99%, and the NYSE Composite fell by 3.02%. The CBOE Volatility Index ascended by 19.78%, suggesting that investors see greater risk in the stock market.

Not everything is bleak in the future of equities. The markets have rallied impressively in the past weeks as stocks rose approximately 11% since October. Bonds have likewise rebounded as interest rates fell significantly from their peak two months ago. The negative prognosis about the economy notwithstanding, the gains in both stocks and bonds are most welcome and provide opportunities for gains even in a pessimistic market. While the declines may be the function of technical factors, it is some concern that the S&P 500 Index recorded its worst return in five weeks even as the small-cap Russell 2000 Index suffered its worst week since late September. The decline in the S&P 500 is a breakdown of its 200-day moving average following the rally. Within this market, the sectors that performed best were health care, consumer staples, and utilities which comprise the defensive stocks. Energy shares sharply fell due to international oil prices descending to their lowest levels since January. Communication services stocks also underperformed due to weakness in Google’s parent Alphabet. Financial shares dropped as a result of negative outlooks offered by several bank executives.

U.S. Economy

The Institute for Supply Management’s (ISM’s) index of services sector activity, which was expected to slightly decrease, defied expectations and rose to 56.5, close to its highs over the past several months. This is a positive indication because readings over 50 suggest expansion in the activity of the services sector. The ISM observed that there is a particular rise in business activity, particularly in real estate and food services and accommodation.

On Friday, the producer price inflation (PPI) data were released, providing a modest surprise on the positive side. The PPI figures rose 7.4% year-over-year, an improvement over consensus expectations of approximately 7.2%, causing stock futures to plunge sharply. The details of the report appear to broadly confirm a continued deceleration in trend inflation, particularly for consumer goods. On the same day as the release of the PPI report, the University of Michigan published its preliminary survey of consumer sentiment for December. The survey results added to the implications from hard data that there is general stability in the near-term outlook for the U.S. consumer. Long-term inflation expectations are unchanged at 3%, which is at the higher end of the historical range for this data, however, short-term inflation expectations had descended further.

The yield on the benchmark 10-year U.S. Treasury note reached close to the three-month intraday low on Wednesday. It closed higher at the end of the week, driven by the PPI data and news that China is easing its strict pandemic restrictions. The strong surge in yields was tempered by the weaker-than-expected unit labor cost data and comments by Russian President Vladimir Putin regarding the mounting risks of nuclear engagement.

Metals and Mining

Some follow-through buying in the gold market is materializing after November’s massive rally. Gold prices end the week close to their four-month high above $1,800 per ounce. While it is not entirely clear of risks, many investors and analysts are considering gold to now be a “buy the dip” asset. It is a marked change from the summer sentiment of gold being a “sell the rally” asset. The short squeeze in November was followed by gains in December, suggesting that gold prices are now in neutral territory for the year with a slight 1% loss. This compares favorably against the S&P 500 which is charting a year-to-date loss of 17%. Most gold investors still consider 2022 a disappointing year, because even in light of the significant rise in inflation, the performance of gold was lackluster. Although gold is an inflation hedge, the headwinds of a strong U.S. dollar overcame the inflation effect as the Federal Reserve was compelled to raise interest rates at the fastest pace in more than four decades. This fact notwithstanding, gold has performed its role as a portfolio diversifier.

Gold moved sideways for the week, beginning at $1,797.63 and ending hardly changed at $1,797.32 per troy ounce (a slide of 0.02%). The same is true with silver which moved up by 1.43% from $23.14 to $23.47 per troy ounce. Platinum, which ended the previous week at $1,019.11, closed trading this week at $1,027.58 per troy ounce, a modest rise of 0.83%. Palladium ended the week before at $1,901.40 and this past week at $1,956.76 per troy ounce, up by 2.91%. The three-month LME prices of base metals ended mostly up. Copper, which was $8,336.00 the week before, closed at $8,543.00 per metric tonne this week for a slight increase of 2.48%. Zinc rose by 5.23% from the week-before close at $3,079.50 to this week’s ending price of $3,240.50 per troy ounce. Aluminum began at $2,485.00 and ended this week at $2,480.50 per metric tonne, sliding 0.18% for the week. Tin, which closed at $23,331.00 one week before but ended this week at $24,290.00 per metric tonne, inched up by 4.11% for the week.

Energy and Oil

The news for the week provided reasons to expect an uptick in oil prices, but due to thin liquidity, the surge did not materialize. The easing of coronavirus restrictions in China should have hinted at a strong economic recovery that will increase demand, and a U.S. oil spill halting pipeline deliveries from Canada would have added to concerns of constricting supply. Additionally, there is a massive queue of tankers that is unable to pass the Turkish Straits, halting deliveries in some areas. A protracted disagreement between Turkish authorities and maritime insurance providers had cast a shadow over the launch of the Russian oil price cap this week, and almost two dozen tankers were stalled on their southbound voyage out of the Black Sea for not having the required P&I insurance documents. Oil prices will likely be unable to close the year on a renewed growth trajectory. It is unlikely that investors who realized profits over the year will risk taking a position in this uncertain environment. Brent may be stalled at $75 to $78 per barrel for longer than expected.

Natural Gas

For the report week beginning Wednesday, November 30, and ending Wednesday, December 7, 2022, the Henry Hub spot price dropped by $2.27, from $6.80 per million British thermal units (MMBtu) at the start of the week to $4.53/MMBtu by the week’s end. The price of the January 2023 NYMEX contract descended by $1.207, from $6.930/MMBtu to $5.723/MMBtu week-on-week. The price of the 12-month strip averaging January 2023 through December 2023 futures contracts slid by $0.677 to $5.032/MMBtu. Also, this report week, international natural gas futures prices increased. Weekly average futures prices for liquefied natural gas (LNG) cargoes in East Asia climbed by $1.97 to a weekly average of $32.98/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, increased by $2.94 to a weekly average of $42.95/MMBtu.

World Markets

Renewed fears of a recession sent European shares southward as central banks further tightened monetary policy to bring inflation under control. The pan-European STOXX Europe 600 Index closed the week 0.94% down in local currency terms. The trend was replicated by major indexes in the region. Italy’s FTSE MIB Index dropped by 1.40%, Germany’s DAX Index descended by 1.09%, and France’s CAC 40 Index dipped by 0.96%. UK’s FTSE 100 Index slid by 1.05% for the week. Economic data revised growth in the eurozone economy to 0.3% from 0.2% sequentially in the third quarter, boosted by increases in household spending and business investment.

In Japan, modest positive returns over the week were realized by the country’s stock markets. The Nikkei 225 Index rose 0.44% and the broader TOPIX Index increased by 0.39%. To some extent, investor sentiment was impacted by economic data showing that the Japanese economy contracted less than first estimated in the third quarter of 2022. Market gains were capped, however, by uncertainty about the trajectory of U.S. monetary policy. the yield on the 10-year Japanese government bond (JGB) closed the week unchanged at 0.25%, although it touched 0.26% briefly due to speculation that the Bank of Japan (BoJ) may abolish its JBG yield cap as soon as next year. The yen slid from JPY 134.3 to about JPY 136.2 against the U.S. dollar week-on-week, due to the continued divergence in the monetary policies of the U.S. Federal Reserve and the BoJ. The Fed is widely expected to continue increasing interest rates while the BoJ has consistently affirmed that it will continue with its ultra-loose policy position.

Chinese equities climbed on the back of Beijing’s rapid easing of coronavirus pandemic restrictions, in turn bolstering investor sentiment despite expectations that infections will rise in the coming months. The Shanghai Composite gained 1.6% and the blue-chip CSI 300 Index ascended 3.3% in its biggest weekly gain since early November. Chinese officials released a 10-point guideline for their new COVID prevention and control measures. These included a vaccination program for the elderly, home quarantine for people with mild symptoms, and reducing mass testing requirements in many cities. In high-risk areas, if no new cases appeared for five consecutive days, lockdowns will be lifted. Analysts and investors remain cautious, however, that China’s quick shift from zero-COVID policies might increase business uncertainty and hamper the economy further if infections and deaths begin to increase.

The Week Ahead

The CPI index, retail sales growth, and jobless claims are among the important economic data scheduled for release this week.

Key Topics to Watch

- NY Fed 1-year inflation expectations

- NY Fed 5-year inflation expectations

- Federal budget (compared with Nov. 2021)

- NFIB small-business index

- Consumer price index

- Core CPI

- CPI (year-on-year)

- Core CPI (year-on-year)

- CPI excluding shelter (3-month rolling annualized rate)

- Import price index

- Federal funds rate announcement

- SEP median federal funds rate for end of 2023

- Fed Chair Jerome Powell news conference

- Initial jobless claims

- Continuing jobless claims

- Retail sales

- Retail sales excluding motor vehicles

- Empire state manufacturing index

- Philadelphia Fed manufacturing index

- Industrial production index

- Capacity utilization rate

- Business inventories

- S&P U.S. manufacturing PMI (flash)

- S&P U.S. services PMI (flash)

Markets Index Wrap Up