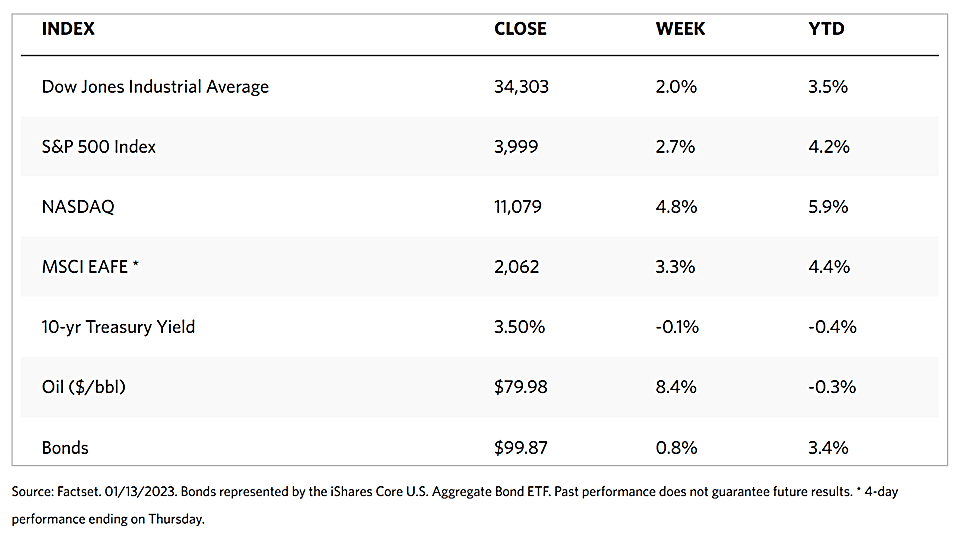

Stock Markets

The stock market chalked up its second straight week of gains, with investors welcoming the good news that inflation data matched consensus estimates and that the quarterly earnings reporting season officially began on Friday. As reported by the Wall Street Journal, the technology tracker Nasdaq Stock Market Composite outperformed with a gain of 4.82%. The Dow Jones Industrial Average climbed 2.00% while the total stock market index ascended by 3.06%. The broad S&P 500 Index rose by 2.67%, and the NYSE Composite added 2.44%. CBOE Volatility descended by 13.16%, signaling investors’ perception of falling risks.

The rally by the Nasdaq Composite and growth-oriented sectors were supported by rebounds in certain mega-cap technology stocks such as Amazon.com, Tesla, and Microsoft. Sectors that lagged included consumer staples. Financial stocks JPMorgan Chase, Wells Fargo, and Bank of America released earnings Friday morning that beat consensus expectations, although cautious outlooks from the large banking corporations triggered a fall in their share prices in early trading.

U.S. Economy

The Labor Department’s report on consumer price index (CPI) inflation on Thursday morning was largely anticipated by investors during the early part of the week. The reports were viewed by Wall Street as benign. In December, headline prices dipped 0.1%, slightly lower than expected. It is also the first decline since May 2020, bringing the year-over-year increase to 6.5%, its lowest level since October 2021. Core consumer inflation, which excludes food and energy, dipped according to expectations, to 5.7%. This is also the slowest pace in more than a year. Largely accounting for the remaining inflation pressures are the ongoing increases in the calculation of shelter costs, which lag actual declines in home prices and rents.

Goods inflation likewise fell for the third straight month, largely driven by the sixth monthly decline in used car prices. This is also the first decline in new car prices in two years. Goods prices are likely to further descend as supply shortages get resolved, the cost of shipping falls, and consumer demand eases. Noticeable is the increase in services inflation, largely due to the increase in shelter, the biggest component of inflation as it accounts for about one-third of the overall index. This component increased the most in three months, although the strength of the movement may be expected to temper. Tending to lead the shelter inflation index by several quarters are new leases and home prices, and it is worthwhile to note that both have been descending in response to the sudden increase in borrowing costs. Housing inflation may be expected to start moderating later in the year, as the data appear to point out.

Metals and Mining

Gold and silver are starting the year on an upward trend, suggesting that bullish sentiment is prevailing in the marketplace. This week gold broke above the $1,900 level and ended the week at $1,920 per ounce, the highest level in nine months, bringing it to 5% higher since the year began, and $300 higher since the precious metal’s two-year low in November. Even now, some analysts and investors are setting their sights on the $2,000 target. At the same time, silver is solidly back above $24 an ounce. Some heavyweight analysts are anticipating that investors will flock to gold as several major threats are likely to descend on the global economy. Furthermore, both bond yields and the U.S. dollar have peaked, trends that supported the gold rally.

According to Bloomberg, gold spot price ended the week at $1,920.23 per troy ounce, an increase of 2.92% from the previous week’s close at $1,865.69. Silver, which closed one week ago at $23.83, ended this week at $24.26 per troy ounce to register an increase of 1.80%. Platinum lost 2.30% from the earlier week’s price of $1,094.33 to this past week’s price of $1,069.21 per troy ounce. Palladium also lost by 1.06%, from the week-ago close at $1,811.93 to this week’s close at $1,792.81 per troy ounce. The three-month LME prices of base metals generally rose for the week. Copper increased from the previous close at $8,589.50 to this week’s close at $9,185.50 per metric tonne, a weekly gain of 6.94%. Zinc ascended from last week’s closing price of $3,023.50 to this week’s closing price of $3,324.00 per metric tonne, a rise of 9.94%. Aluminum prices went up by 13.05% for the week, from $2,295.50 one week ago to $2,595.00 per metric tonne this week. Tin, which ended last week at $25,270.00, closed this week at $28,756.00 per metric tonne, for a gain of 13.80%.

Energy and Oil

Much uncertainty presently pervades the oil markets, especially concerning the timing of the demand recovery of China as it gradually moves away from its zero-Covid policy. Even in the face of this uncertainty, oil prices have risen on the back of the easing of U.S. inflation data and consumer prices descending for the first time in the last two and a half years. WTI is once more moving toward the $80 per barrel price threshold, and Brent is approaching $85 per barrel. In local news, the U.S. passed a broadly bipartisan bill that would limit direct sales of oil from the Strategic Petroleum Reserve to China, similar to what had taken place in the 180-million-barrel emergency release last year. Also developing are the plans by the U.S. National Highway Traffic Safety Administration to propose this April new fuel economy standards for 2027 and beyond.

Natural Gas

The U.S. natural gas production surged to its highest level on record in 2022. This is attributable to three causes: the continued decline in drilled but uncompleted wells; higher rig counts surpassing March 2020 levels; and, increased takeaway capacity to supply Gulf Coast liquefied natural gas (LNG) terminals. In the weekly report covering Wednesday, January 4, to Wednesday, June 11, 2023, the Henry Hub spot price fell by $0.46 from $3.81 per million British thermal units (MMBtu) at the start of the week to $3.35/MMBtu at the end of the week. The price of the 12-month strip averaging February 2023 through January 2024 futures contracts descended by $0.348 to $3.748/MMBtu.

International natural gas futures prices declined for this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia came down by $1.63 to a weekly average of $27.67/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, decreased by $1.17 to a weekly average of $22.02/MMBtu. In the same week last year (the week ending January 12, 2022), the prices in East Asia and at TTF were $33.44/MMBtu and $28.18/MMBtu, respectively.

World Markets

European shares rallied for the second straight week due to the better-than-expected economic data that raised hopes of a brief and shallow recession. Market optimism was tempered, however, by sentiments of some central bankers that interest rates would need to be hiked further. The pan-European STOXX Europe 600 Index closed the week higher by 1.88% in local currency terms. Major stock indexes in the region surged. Germany’s DAX Index climbed by 3.26%, France’s CAC 40 Index ascended by 2.37%, and Italy’s FTSE MIB Index added 2.40%. The UK’s FTSE 100 Index advanced by 1.88%. The Eurozone unemployment rate remained steady at 6.5% in November, which is consistent with economists’ expectations. Investor morale, meanwhile, strengthened for a third straight month in January. The economic sentiment index compiled by Sentix rose to its highest level since June of 2022, although it remains in negative territory. Eurozone data published earlier this month showed economic sentiment improved in December for the first time since Russia first invaded Ukraine.

Japan’s equities climbed during the week, as investors’ risk appetite rose with the weakening momentum in the U.S. consumer price inflation. The Nikkei Index ascended by 0.56% and the broader TOPIX Index rose by 1.46%. The slowdown in the U.S. CPI announced during the week raised hopes that the U.S. Federal Reserve would slow the pace of its interest rate hikes. On the other hand, core consumer price inflation in Tokyo jumped by 4.0% year-on-year in December. This was the fastest rate increase experienced in the past 40 years, fueling speculation that the Bank of Japan (BoJ) may revise its inflation forecasts upward and evaluate the feasibility of further monetary policy adjustments when it next meets on January 17-18. Contrary to expectation, the BoJ adjusted its yield curve control (YCC) framework last month. As a result, the BoJ was again compelled to conduct unscheduled bond-buying operations to maintain the 10-year Japanese government bond (JGB) yield at around its new 0.50% cap, approximately at the level at which it ended this week. The yen firmed up to about JPY 128 versus the U.S. dollar, from around JPY 132 to the greenback the week before.

Chinese stocks gained ground upon the announcement of a lower-than-expected U.S. inflation rate even as optimism was boosted by the post-pandemic reopening outlook. The Shanghai Composite Index advanced 1.19% and the blue-chip CSI 300 gained 2.35%, the highest it has seen in four months. After Beijing abandoned its zero-covid policy in December and officials accelerated measures to support the troubled property sector, hopes increased that the domestic demand will recover in the coming months. China issued a large quota for crude oil imports earlier in the week to prepare for what they expect will be an increase in energy demand resulting from the economic recovery that follows the waning infection rate. Economists project that China’s economy will experience a swift rebound once infections peak, and foresee a 4.9% growth for 2023 as against an estimated growth rate of about 3% in 2022. China’s exports dropped 9.9% in December compared to one year earlier, due to softening global demand and rising infections disrupted activity. Inflation gained momentum, rising 1.8% in December. Core inflation, which excludes food and energy prices, rose slightly after it remained unchanged for three straight months.

The Week Ahead

The PPI Index, Retail Sales growth, and initial and continuing jobless claims are among the important economic data scheduled for release in the coming week.

Key Topics to Watch

- Empire State manufacturing index

- Retail sales

- Retail sales ex motor vehicles

- Producer price index, final demand

- Industrial production

- Capacity utilization

- NAHB home builders’ index

- Business inventories (revision)

- Beige book

- Initial jobless claims

- Continuing jobless claims

- Building permits (SAAR)

- Housing starts (SAAR)

- Philadelphia Fed manufacturing index

- Fed Vice Chair Lael Brainard speaks

- Existing home sales (SAAR)

- Fed Gov. Christopher Waller speaks at Council on Foreign Relations

Markets Index Wrap Up