Stock Markets

Stocks pulled back as yields moved up, continuing the cycle of volatility of preceding weeks. During the week two emerging perceptions appear to prevail among investors. One is the view that high interest rates and high stock prices are simply incompatible and one must prevail. Second is the view that the decline in stocks has been significant enough to signal that the market is taking off in a new direction. Both views have merit but are somewhat overstated. Regarding the first perspective, although rates are higher, they are not high in retrospect. Ten-year rates have merely returned to their levels one year ago. The 20-year average of the ten-year interest rates is 3.1%, double the current 1.6%, thus the present level is nowhere near historical highs. The second view, that the market is entering a “sell-off” or “turmoil” as headlines predict, can hardly be substantiated given that the S&P 500 slid by only 3.4% from Monday’s closing high to Thursday’s closing low.

U.S. Economy

The recent market sentiment does appear to be changing from the sharp and steady climb it experienced over the past year. Concerns of rising interest rates and inflationary pressures have largely replaced talk of stimulus and reopening. That being said, it does not appear that the market has already peaked at the present. Broader economic measures, however, do not appear to support this position.

- The Fed is far from adopting a monetary policy that may lead to overtightening in the economy. The stimulus measures are still in effect and the policy rate has not yet undergone any upward adjustment. Any increase in inflation is taken as a sign of a recovering economy, particularly in light of the deep recession it has just been through. Eventually, rates will have to increase to more restrictive levels, but this may be years in the future. What is currently taking place is a recalibration process that has long influenced the interaction between the Fed and the stock market.

- The labor market is still on the road to recovery. The February employment report released last Friday shows that 379,000 jobs were added to the U.S. economy, more than double the gains in January, with the best payroll growth in the last four months. It is heartening to observe that of the new jobs added, 355,000 were in hospitality and leisure, indicating a comeback in this most depressed segment of the economy. It could only portend stronger performance particularly for small businesses and the services sector as vaccinations are deployed and restrictions are lifted.

- There is still significant upside in the labor market. Although 12.9 million jobs have been added since May, the employment level is still 9.5 million short of pre-pandemic employment figures. This points to further job recovery and more job creation, a leading driver in the economic recovery. It will further boost consumer confidence and aggregate income which, combined with the already increased level of personal savings, may just fuel average household spending and GDP growth for the year.

Metals and Mining

For the first time since June 2020, gold slid below $1,700 per ounce, continuing its decline after beginning the month at $1,735. Global gold ETFs fell 84.7 tonnes in February, historically the seventh-worst month for losses. Some upside is expected in the future, however, as the movement appears to form part of a correction that may soon see the bottom before recovering lost territory. As of Friday, gold was trading at $1,698.44. Silver also saw a pullback in the first week of March following a month of slow but steady gains. Part of the price drop was due to the metal’s correlation to gold, although it was buoyed by robust industrial demand and strong investor interest. The price held above $25 per ounce, trading at $25.02 on Friday.

Platinum peaked at a six-year high, breaking out at $1,212 per ounce at the start of the week’s trading, but subsequently dropping to $1,108 on Thursday. It recovered to trade at $1,113.30 on Friday. Palladium is the only precious metal to buck to trend downwards. It realized a modest 0.05% gain, rising from $2,261 to $2,274 per ounce over the week, and trading at $2.257 on Friday. It will continue to be sustained by demand in the automotive sector.

Base metals ended up mixed for the week. Copper continues to consolidate at the $8,700 range after hitting a 10-year high in February when it traded above $9,000 per tonne for the first time since 2011. Further demand may still boost the red metal as its antiviral properties are highlighted and supply remains tight. Nickel, on the other hand, plunged 13.4%. It faces a price recovery, however, as supply faces some constraints due to the suspension of operations in Guatemala’s Fenix nickel mine in light of environmental concerns. Nickel was trading at $16,144 per tonne on Friday. Prices for zinc and lead also saw a correction from their gains in February. Zinc closed the week at $2,734.50 per tonne, lead at $2,014 per tonne.

Energy and Oil

The price of oil continues on its steep uptrend as OPEC+ decided to suspend plans to ease production cuts for one more month. This caught the oil market off-guard as expectations for an easing in the oil supply situation were dashed. Even Saudi Arabia announced that it would continue to keep in place its 1 mb/d of voluntary oil cuts. The market reacted to the unexpected news with a sudden surge in prices.

As oil prices continue to rise and drillers are tempted to return from the sidelines, the shale business may likely return to aggressive production levels. As the markets get to the $70-$75 per barrel oil range, the prospects for strong growth are enhanced even with returns to investors becoming increasingly lucrative. This only entices shale producers to take advantage of the bullish market conditions. Further providing an incentive for the continued oil price increase is Biden’s moratorium on new drilling in federal lands. While this does not have an immediate impact, it is likely to curb production by anywhere between 230,000 to 490,000 bpd by the end of 2025.

Natural Gas

At most locations this week, natural gas prices remained relatively steady, rising only less than $0.10 per million British thermal units (MMBtu) at most hubs. The Henry Hub spot prices rose from $2.75/MMBtu on the Wednesday of the previous week to $2.85/MMBtu last Wednesday. The March 2021 contract expired last Wednesday at the New York Mercantile Exchange (NYMEX) at $2.854/MMBtu, while the April 2021 contract price increased by $0.02/MMBtu to $2.816/MMBtu. The price of the 12-month strip averaging April 2021 through March 2022 futures contracts rose to $2.988/MMBtu, up by $0.02/MMBtu.

World Markets

European shares rose on investor optimism that vaccine deployment will lead to an easing of restrictions to curb the coronavirus spread and that monetary and fiscal policies will be adopted to support the economy’s reopening efforts. The rise was tempered by sentiments that central banks will likely adopt measures to contain the possible increase in inflation rates. The pan-European STOXX Europe 600 Index climbed 0.91%, in tandem with major stock indexes. The UK’s FTSE 100 Index rose 2.27% this week, prompted by the release of finance minister Rishi Sunak’s annual budget calling for more fiscal stimulus. A further incentive was provided by projections from the Office for Budget Responsibility that the economy is likely to recover to pre-pandemic levels earlier than first projected.

In Germany, German Chancellor Angela Merkel extended lockdown restrictions until March 28, but at the same time eased containment measures in areas with reduced infection rates. Bookshops, some stores, garden centers, florists, museums, and art galleries were allowed to resume business. Italy blocked the shipment of 250,000 doses of the Oxford-Astra Zeneca coronavirus vaccine originally scheduled to be shipped to Australia. This is the first intervention of any country in the EU since rules were adopted regarding the shipment of vaccines outside the bloc. France may also block vaccine shipments outside the EU. The EU may likely impose export controls on vaccines until the end of June.

In Japan, the stock markets ended mixed for the week. The Nikkei 225 Stock Average declined 0.35% while the broader TOPIX Index rose 1.70%. The yen softened to close above JPY 108 against the U.S. dollar, and the yield of the 10-year Japanese government bond closed the week at 0.09%, its lowest level since the middle of February. Some positive news helped sustain the market as it was reported that the Japanese manufacturing sector expanded in February for the first time in nearly two years. However, the services sector saw a further slump in light of the continued coronavirus restrictions. In the meantime, Chinese shares fell in volatile trading as nervous sentiments concerning the U.S. rising yields and inflation expectations spilled over onto the country’s bourses. The large-cap CSI 300 Index slid 1.4% while local currency A shares declined 0.2%. Technology shares fell on the back of weakness in prominent companies in the consumer, electric vehicles, and property management sectors. The yield on China’s sovereign 10-year bond rose to end the week at 3.36%, while the renminbi remained unchanged against the U.S. dollar.

The Week Ahead

Important reports scheduled for release in the coming week include consumer sentiment, inflation data, and initial claims.

Key Topics to Watch

- Wholesale inventories

- NFIB small-business index

- Consumer price index

- Core CPI

- Federal budget

- Initial jobless claims (regular state program)

- Continuing jobless claims (regular state program)

- Job openings

- Prudence price index final demand

- UMich consumer sentiment index (preliminary)

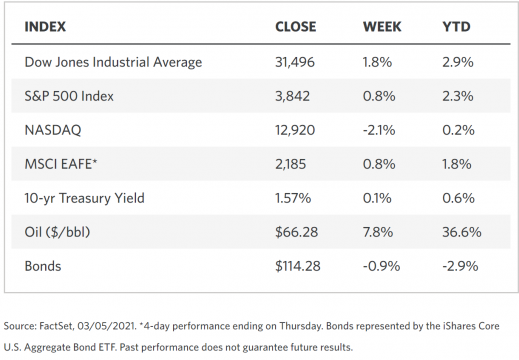

Markets Index Wrap Up