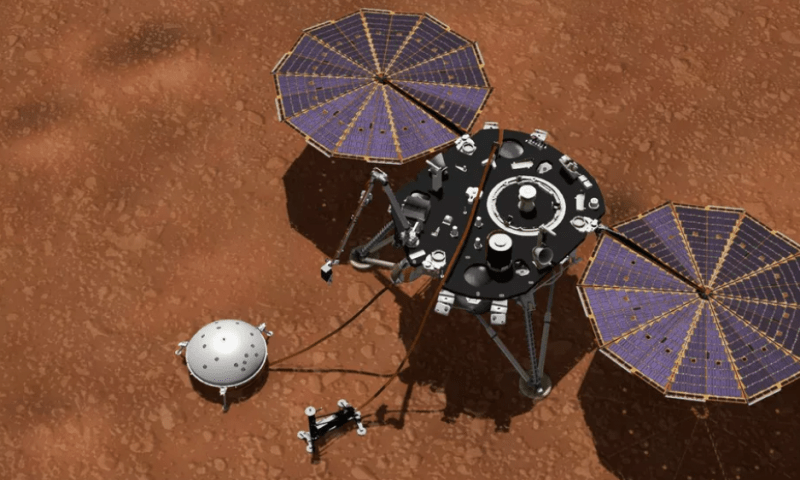

Several reports coming from Japan are announcing that Tesla and Panasonic are ending their solar cell production deal at Gigafactory New York ahead of Elon Musk holding an event at the factory.

Back in 2017, Tesla made another manufacturing agreement with Panasonic to accelerate the production of solar products at the factory it inherited from SolarCity in Buffalo following the acquisition of the company.

They called the factory Gigafactory 2 because they aim to produce over 1 gigawatt of solar products at the factory, which also happens to work under a similar deal as Gigafactory 1, where Tesla and Panasonic manufacture batteries.

Panasonic invested in the production of solar cells at te factory, which has recently been renamed Gigafactory New York, and Tesla agreed to buy those cells to put inside the solar roof tiles, now called Solarglass, that it itself manufactures at the location. Panasonic is also separately producing solar modules at Gigafactory New York, for Tesla’s solar retrofit business.

The deal hasn’t panned out exactly as planned.

Tesla hasn’t been buying a lot of solar modules from the plant and its solarglass production ramp has been extremely slow.

Furthermore, Tesla has reportedly been using solar cells from other manufacturers in its solar roof tiles.

Now reports from Reuters and Nikkei both states that Tesla and Panasonic are ending their solar cell production deal at the factory in New York.

Nikkei reported today

“Tesla and Panasonic are scrapping their partnership in producing solar cells after years of struggling to ramp up output at the Gigafactory 2 in upstate New York.”

The deal at Gigafactory Nevada to produce battery cells for Tesla’s Model 3 and Model Y is reportedly intact. The report also states that Tesla is considering bringing new production to Gigafactory New York and they are not expecting to have issue fulfilling their employment requirements with the state, which paid for the factory.

We contacted Tesla about the reports and we will update if we get more information.

The news comes soon after Elon Musk announced a ‘Tesla April company talk’ to be held at Gigafactory New York and it is expected to be related to Tesla’s previously announced ‘Battery Investor Day’, which should involve a new battery announcement.

When announcing the event, Musk also said that Tesla will be expanding solar roof installs internationally and that it will become an important product for the company.

The past week has been volatile for Bitcoin, and yesterday was no exception. In the evening, BTC bulls were able to push the cryptocurrency up to highs of $10,000 before it faced a swift rejection that has led it to grind lower today.

The crypto’s inability to gain any stability within the five-figure price region certainly does seem to spell trouble for bears, but it is important to keep in mind that sellers have not been able to catalyze any sustained downwards movement throughout the course of BTC’s 2020 uptrend.

Now, one economist is noting that BTC still has a significant way to fall before it enters bear market territory, explaining that the strength of its recent uptrend is likely to extend further.

Bitcoin Stabilizes Around $9,620 as Resistance Continues Mounting

At the time of writing, Bitcoin is trading down just under 3% at its current price of $9,630, which marks a notable decline from daily highs of just over $10,000 that were set yesterday in the minutes following the cryptocurrency’s weekly close.

This bullishness was short-lived, as the rejection at this level sparked a selloff that cut as deep as $9,500 before bulls stepped up and began absorbing the selling pressure.

In the near-term, Alex Krüger, an economist who focuses primarily on cryptocurrency, explained that he believes the sub-$9,000 area is an attractive region for “shorts to target and longs to open,” meaning that this may be where it dips to before finding enough buying pressure to catalyze its next uptrend.

“Area below 9K is very attractive for shorts to target and longs to open. Excessive leverage has been largely rinsed out. Bigger picture players are still looking at new year highs. I still expect higher prices prior to the halving and think once 10300 breaks should see 11K soon,” he explained in a tweet from his alt account.

BTC Could Dip Significantly Further Before Its Bull Market Falters

It is important to keep in mind that even a drop to sub-$9,000 may not be enough to invalidate the cryptocurrency’s bullish market structure.

Krüger further noted in a later tweet that he does not believe the benchmark crypto’s recent price action is the start of a bear trend, and that a shift in market structure will only occur once it breaks below the mid-$8,000 region, as this is where its trend shifted during the volatility seen last October.

“I do not find reason to believe this is the beginning of a bear trend, even if price were to break down. Here’s an example. On the October China move, the uptrend only failed once $BTC got into the 8200-8000 area. Until then, the correction lower was a simple pullback,” he noted.

Although it does remain a strong possibility that Bitcoin’s price will see some further near-term downside, bears have significant work cut out for them if they want to invalidate BTC’s firm 2020 uptrend.

A major effort to expand development of Canada’s oil sands has collapsed shortly before a deadline for government approval, undone by investor concerns over oil’s future and the political fault lines between economic and environmental priorities.

Nine years in the planning, the project would have increased Canada’s oil production by roughly 5 percent. But it would have also slashed through 24,000 acres of boreal forest and released millions of tons of climate-warming carbon dioxide every year.

Some Canadian oil executives had predicted that Prime Minister Justin Trudeau and his cabinet would approve the project by a regulatory deadline this week, though with burdensome conditions. But in a letter released Sunday night, the Vancouver-based developer, Teck Resources, declared that “there is no constructive path forward.”

The unexpected withdrawal relieves Mr. Trudeau of a choice that was sure to anger environmentalists or energy interests, if not both.

Conservatives were quick to blame Mr. Trudeau for the loss of a project that they said would have created thousands of jobs and given an economic lift to the western province of Alberta, the hub of Canada’s energy industry, which has suffered from low oil prices over the last five years. They suggested that the government felt pressure from weeks of protests by Indigenous groups opposing a natural gas pipeline, even though some Indigenous groups supported the Alberta project, known as the Frontier mine.

“It is what happens when governments lack the courage to defend the interests of Canadians in the face of a militant minority,” Alberta’s premier, Jason Kenney, said in a statement.

The chief executive of Teck Resources, Don Lindsay, said in a letter to federal officials that global capital markets, investors and consumers were looking to governments to put “a framework in place that reconciles resource development and climate change, in order to produce the cleanest products” — something that he said “does not yet exist here.”

While environmental concerns were part of government and company calculations, there was no guarantee that the Frontier project would have gone forward even if it gained final regulatory approval. Mr. Lindsay had said the company needed a deep-pocketed partner to help pay for the project, and higher oil prices.

Canada supplies nearly six million barrels of oil a day, making it the world’s No. 4 producer and the biggest source of American imports. The oil sands contribute over 60 percent of that output and are vital to the west’s economy. Canadian output continues to grow because of investments made when global supplies were tighter.

The oil sands are a watery mixture of sand and clay soaked with a dense, viscous form of petroleum known as bitumen. But in addition to being a fossil fuel, bitumen is difficult to extract and energy-intensive to process.

And when Teck Resources proposed the Frontier project, the energy world was very different. The American shale-drilling frenzy was in its infancy, and the Keystone XL pipeline was seemingly going to deliver the oil-sands output to the American market.

Now the United States has an abundance of relatively cheap oil, prodigious deposits are being tapped in Brazil, Norway and Guyana, and the Keystone project is still awaiting completion. Delays in pipeline approvals have prompted the Alberta government to mandate production cutbacks over the last two years to drain a glut of oil in storage.

Kevin Birn, a vice president and oil-sands expert at the consultancy IHS Markit, estimated that for a project like Frontier to break even, the price of West Texas intermediate oil, the North American benchmark, would need to average $65 a barrel over a decade or more of operations. That is roughly $15 above the current price, and other analysts put the break-even figure at $80 to $85.

But until Sunday night, despite a regulatory review that cost it hundreds of millions of dollars, Teck Resources refused to give up. The company argued that its project, at a cost of 20.6 billion Canadian dollars ($15.5 billion), would create 7,000 construction and 2,500 operational jobs and eventually generate more than 70 billion Canadian dollars in local and national government revenue.

Andrew Leach, a professor of energy economics at the University of Alberta, said some might read the project’s demise as a fatal blow to oil-sands development, but he interpreted Teck Resources’ decision as a pragmatic one.

“Teck was clear that it does not want a situation where one project has to answer for all of Canada’s climate policies and climate commitments,” he said. Moreover, he added, “global investors are not prepared to help a company the size of Teck to build a multibillion-dollar project. The global market was not prepared to be part of the political football.”

No new oil-sands mine has opened since 2018, but more than a dozen proposals are awaiting regulatory approval or investment decisions. Mr. Leach said some of those were economically and environmentally more viable than the Frontier project.

But resistance to new pipelines and high production costs have steadily reduced investments in oil-sands fields. There has been an exodus of international oil companies, including ConocoPhillips, Royal Dutch Shell and Equinor of Norway.

At the same time, there are questions about the market outlook. While world demand is roughly 100 million barrels a day, a figure that increases by 1 percent every year, the International Energy Agency projects that growth will begin to slow considerably in 2025. The agency says demand could fall to 67 million barrels a day in 2040, especially if governments increase regulation and electric cars become commonplace.

Reduced demand would focus production on places where it is cheapest, like Saudi Arabia.

“Companies like Teck are realizing that global capital markets are changing rapidly,” said Simon Dyer, executive director of the Pembina Institute, a leading Canadian environmental research organization. “There was never an economic pathway for this project under global demand scenarios consistent with the Paris climate agreement.”

A federal-provincial panel that reviewed the project, he said, “didn’t properly assess the climate impacts.” The national parks agency also raised concerns about the possible effect on a national park downstream that is a UNESCO world heritage site.

The Alberta Energy Regulator wrote in July that “there will be significant adverse project and cumulative effects on certain environmental components and Indigenous communities.” Nevertheless, it approved the project after finding it in the public interest.

Two federal officials — Environment Minister Jonathan Wilkinson and Natural Resources Minister Seamus O’Regan — issued a joint statement welcoming Teck’s decision. “A strong economy and clean environment must go hand in hand,” they said.

NASA’s InSight lander has detected hundreds of “marsquakes” on Mars, including about 20 tremors that were relatively significant. Compared to quakes here on Earth, the marsquakes were pretty puny, but the new data could provide planetary scientists with more information about the interior of Mars.

The initial results of the mission were published on Monday in the journals Nature Geoscience and Nature Communications. The lander, which touched down on Mars via supersonic parachute in 2018, detected its first possible marsquake in April 2019.

Many of the quakes that InSight detected were small enough that they probably wouldn’t be felt if they happened on Earth, Philippe Lognonné, principal investigator for one of the lander’s instruments, said in a press conference. “Mars is a place where we can probably say the seismic hazard is extremely low,” Lognonné added. “At least at this time.”

The 24 largest quakes discussed in the paper only reached a magnitude 3 or 4, which on Earth, might be powerful enough to be felt as a rumble on the ground but usually aren’t strong enough to cause serious damage. But unlike on Earth, where quakes can happen closer to the surface, it appears that the marsquakes InSight detected tended to originate far deeper in the planet (30 to 50 kilometers). The deeper the quake, the less shaking is felt on the surface.

The researchers had hoped to register larger quakes, which would have given them a more detailed look at the interior of the planet — and even potentially the core — but that hasn’t happened yet.

“The general cause of marsquakes is the long-term cooling of the planet,” Bruce Banerdt, InSight principal investigator, said in a press call on Friday. The interior of Mars, like Earth, has been cooling down since it was formed. As the planet cools down, Banerdt says, it contracts and the brittle crust of the planet cracks, causing the surface to shudder.

That’s the general outlook, but the specific cause of each quake is still unknown. “The details of the particular mechanisms for these quakes is still for us a mystery,” Banerdt says. “We don’t have any conclusions of the mechanisms on any individual quakes yet.”

They may not know what drives each quake, but they’ve measured a lot of them. In the papers, the authors discuss data from 174 marsquakes collected before September 30th, 2019. Since then, the instrument on board InSight that measures quakes has detected about 450 rumblings. NASA says the “vast majority” of these are probably quakes.

Other sensors were also working while InSight’s seismometer was registering quakes. One detected thousands of whirlwinds near the lander, while another recorded strong magnetic signals coming from underground rocks. Another instrument, a self-hammering probe that was supposed to measure the interior temperature of Mars, hasn’t been as lucky. It was supposed to burrow into the surface, but it encountered trouble last fall when it popped back out of the planet. As a last-ditch attempt to salvage this part of the mission, NASA plans to try to push the probe into the surface in late February and early March.

InSight’s mission lasts for nearly another year, and the team here on Earth will continue to gather more data about the inner workings of the Red Planet until then.

At least a few executives at major automakers have indicated that electric cars are the way of the future, and several of them are making big bets on battery-powered vehicles.

But at least in the United States, the market seems to belong almost entirely to Tesla.

The California carmaker’s Model 3 midsize sedan far outstripped sales of any other competitor in 2019. The next best-selling model that year was the Chevrolet Bolt, which sold a mere 16,000.

The success of both Tesla cars, and Tesla shares, have baffled many in the automotive industry, who point to the company’s small size; precarious financial history; and repeated struggles with manufacturing delays; and customer complaints about long waits for orders and difficulty obtaining parts and service.

Meanwhile established automakers with brands that play at practically every price point and in every segment have been promising and slowly releasing their own stabs at a viable electric vehicle. But none have so far proven to be Tesla killers.

A slew of new models are scheduled for release starting in early 2020, and many are starting to offer specs competitive with what buyers can find on Tesla models. For example, Ford’s Mach-E Mustang electric crossover promises 300 miles of range in one configuration, close to the 322 miles on the long range version of the Model 3 sedan.

But relatively few buyers in the United States seem interested in battery electrics, and industry watchers think many buyers are early adopters buying Teslas out of an interest in the brand or an interest in cutting edge technology, rather than out of an interest in owning an electric car.

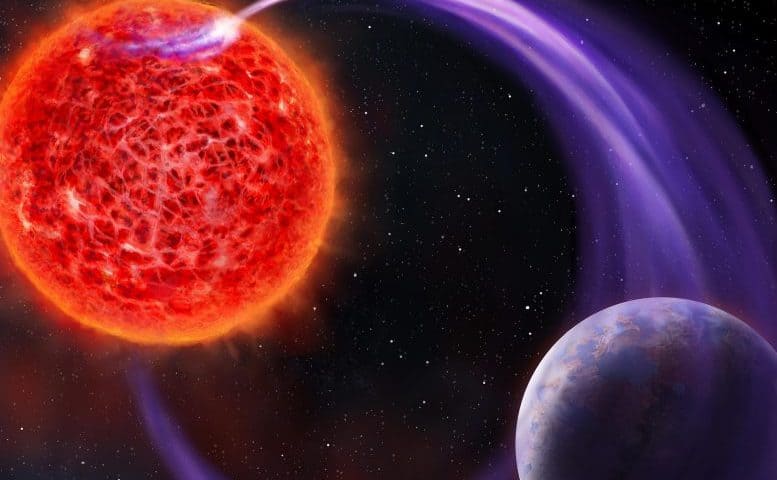

Radio telescope in the Netherlands captures habitats of planets outside our solar system.

A team of scientists using the Low Frequency Array (LOFAR) radio telescope in the Netherlands has observed radio waves that carry the distinct signatures of aurorae, caused by the interaction between a star’s magnetic field and a planet in orbit around it.

Radio emission from a star-planet interaction has been long predicted, but this is the first time astronomers have been able to detect and decipher these signals. The discovery paves the way for a novel and unique way to probe the environment around exoplanets — planets that orbit stars in other solar systems — and to determine their habitability.

Notably, follow-up observations with the HARPS-N telescope in Spain ruled out the alternate possibility that the interacting companion is another star as opposed to an exoplanet.

The work appears in articles in Nature Astronomy and Astrophysical Journal Letters (ApJL).

The breakthrough centered on red dwarfs, which are the most abundant type of star in our Milky Way — but much smaller and cooler than our own Sun. This means for a planet to be habitable, it has to be significantly closer to its star than the Earth is to the Sun.

Red dwarfs also have much stronger magnetic fields than the Sun, which means that a habitable planet around a red dwarf is exposed to intense magnetic activity. This can heat the planet and even erode its atmosphere. The radio emissions associated with this process are one of the only tools available to probe the interaction between such planets and their stars.

“The motion of the planet through a red dwarf’s strong magnetic field acts like an electric engine much in the same way a bicycle dynamo works,” says Harish Vedantham, the lead author of the Nature Astronomy study and a Netherlands Institute for Radio Astronomy (ASTRON) staff scientist. “This generates a huge current that powers aurorae and radio emission on the star.”

Thanks to the Sun’s weak magnetic field and the larger distance to the planets, similar currents are not generated in the solar system. However, the interaction of Jupiter’s moon Io with Jupiter’s magnetic field generates a similarly bright radio emission, even outshining the Sun at sufficiently low frequencies.

“We adapted the knowledge from decades of radio observations of Jupiter to the case of this star,” says Joe Callingham, ASTRON postdoctoral fellow and co-author of the Nature Astronomy paper. “A scaled-up version of Jupiter-Io has long been predicted to exist in star-planet systems, and the emission we observed fits the theory very well.”

To be sure, the astronomers had to rule out an alternate possibility — that the interacting bodies are two stars in a close binary system instead of a star and its exoplanet. The team searched for the signature of a companion star using the HARPS-N instrument (High Accuracy Radial Velocity Planet Searcher) on the Italian Telescopio Nazionale Galileo on La Palma, Spain.

“Interacting binary stars can also emit radio waves,” notes Benjamin Pope, NASA Sagan Fellow at New York University and lead author of the ApJL paper. “Using optical observations to follow up, we searched for evidence of a stellar companion masquerading as an exoplanet in the radio data. We ruled this scenario out very strongly, so we think the most likely possibility is an Earth-sized planet too small to detect with our optical instruments.”

The group is now concentrating on finding similar emission from other stars.

“We now know that nearly every red dwarf hosts terrestrial planets, so there must be other stars showing similar emission,” observes Callingham, also a co-author of the ApJL paper. “We want to know how this impacts our search for another Earth around another star.”

“If we find that most red dwarf planets are blasted by intense stellar winds, this is bad news for their habitability,” Pope, part of NYU’s Department of Physics and Center for Data Science and a co-author of the Nature Astronomy paper.

The group expects this new method of detecting exoplanets will open up a new way of understanding the habitat of exoplanets.

“The long-term aim is to determine what impact the star’s magnetic activity has on an exoplanet’s habitability, and radio emissions are a big piece of that puzzle,” says Vedantham, also a co-author of the ApJL paper. “Our work has shown that this is viable with the new generation of radio telescopes and put us on an exciting path.”

Eat up! A new study says enjoying a big breakfast in the morning can actually help you burn more calories throughout the day.

The new research published in the Journal of Clinical Endocrinology and Metabolism studied a group of healthy young men with a normal body mass index and found the number of calories burned was much higher when they ate a bigger breakfast and a small dinner.

Test results showed they burned more than twice as many calories than those who ate a small breakfast and a large dinner.

Scientists concluded “diet-induced thermogenesis,” the amount of energy it takes to process a meal was higher in the morning than at night.

Although the study showed more calories burned, researchers say this only accounts for about 15% of the total daily calories burned.

Those who are looking to lose weight must also watch what they eat, not just when they eat.

When is the best time to plan for a stock sell-off? When the indices are hitting new highs, of course.

Rarely do investors consider defensive moves in their 401(k)s when stocks are rallying, but that is precisely when you should begin thinking about diversifying your investments.

When stocks get squirrely, I recall a comment from my old colleague, Noel, who used to declare, ‘Well, it’s either the warning bell or the dinner bell.’ More often than not, as we have discussed in previous columns, it’s the dinner bell.

From the time I began investing in 1987 through last year, stocks, as measured by the Dow Jones industrial average, have generated positive returns in 27 of 33 years, or 82% of the annual periods over that time span. That stretch includes Black Monday in 1987, when I began my career, the 2000-2002 market slide and the bear market in 2008 through March 2009.

All of that proves that stock sell-offs usually provide a golden opportunity to heap more holdings onto your plate at lower prices. By the way, the cumulative total return from Jan. 1, 1987, through the end of last year was 3,415%.

An event like Black Monday, my friends, was an epic dinner bell.

Buy low, sells high with your 401(k)

If you, like me, believe stocks are still in a long-term bull market, then meaningful downturns (think Q4 2018) provide a happy opportunity to look at our 401(k) contributions and allocations with new eyes. The hardest part of investing is to be a buyer of stocks in a falling market and a seller in a rising one. It just feels wrong. But it works.

When stocks begin their inevitable slide (markets experience a correction of 5% to10% in just about every annual period), increase your contribution level to your 401(k). It simply makes sense to buy more of something when it is cheaper. You can dial your contribution back once the market rallies if you must, but you will have used the weakness to increase your purchasing power. This will be a powerful contributor to total over a 401(k) lifetime.

Dividend-paying stocks

Add a fund that invests in dividend-paying stocks with proceeds from your soaring growth fund. The most important consideration is a fund that invests in companies that grow their dividend each year. No longer just associated with electric utilities and industries that grow when the economy is strong – dividends are now paid by technology companies like Microsoft and Apple as well as those like Starbucks and McDonalds that have long been categorized as growth stocks. The advantage of investing in these stocks is that the companies tend to grow the dividend faster than the traditional dividend payers. A second advantage is the power of compounding growing dividends enhances total return and provides natural protection in declining markets.

Rebalancing your allocations

Don’t forget the rest of the globe. The U.S. is frequently the best house on the global block. But global markets can provide additional diversification and total return. This may be a good place to invest when U.S. stocks are hitting historical highs.

You should also rebalance holdings that have appreciated far above the initial target you selected. Outperformance is good. But you don’t want the market making your asset allocation decisions for you. If you determined to place 50% of your 401(k) in a particular fund, allow it to run, but if it gets to be more than 10%-15% above your initial allocation, trim it back and transfer the money to a fund that offers fresh diversification or may have lagged recently. Again, you are increasing your purchasing power.

It is true that being invested through good years and bad provides a compelling total return. Never succumb to the siren song that convinces us when stocks are rising that they will continue to do so. Nor should you yield to the temptation to sell out when stocks are declining. Having sold stocks at the end of the painful bear market of 2008 would have cost you the opportunity to enjoy the 333% that stocks returned (again as measured by the DJIA) from Jan. 1, 2009, through last year.

Your 401(k) is meant to be invested for the long term. But you should be an active participant in your future. Consider the old investing maxim that exhorts investors to buy low and sell high. Tuning out the noise will allow you make important adjustments to your investments at turning points.

Cryptocurrency markets are on the move again: Category giant bitcoin has seen its tokens gain 40% in value in 2020 alone, and 155% over the last 52 weeks. If bitcoin was a stock, the “company” would be worth roughly $185 billion today. That market cap would land it right between aerospace titan Boeing and software giant Adobe as one of the 40 most valuable companies on the U.S. stock market.

Bitcoin’s founders and supporters see it as “a new kind of money.” As such, market watchers on both the bull and bear sides of the cryptocurrency debate often argue that the tokens — currently trading in the neighborhood of $9,700 each — will either skyrocket in value to at least $1 million, or bitcoin will collapse and die. There is no middle ground.

If bitcoin achieves a large enough scale and a wide enough acceptance to become a viable alternative to gold, silver, or national currencies as a value store, the cryptocurrency will have a bright future. If not, it’s supposedly heading to zero in the end. The same goes for many other cryptocurrencies, and hundreds of them have already crashed and burned.

Pictures speaking volumes

So how big is the total cryptocurrency market as a value store today? Surprisingly small, actually:

The stock and bond markets make the others look tiny. Let’s zoom in on the precious metals and cryptocurrencies alone:

Yeah, it’s still difficult to see bitcoin and its crypto-peers next to the mountain of gold. I was surprised to see the relative lack of value in silver, but while modern mining companies extract more than 10 times as much silver every year than gold, ounce for ounce, gold is close to 90 times more valuable. And less than 5% of all the silver ever mined is in an investable form today — coins or bullion. The rest has been used for jewelry, decoration, or by industry — and a fair share of it has essentially been lost. You learn something new every day.

What’s next?

So where does this leave the cryptocurrency discussion? Well, neither bitcoin nor the crypto market as a whole stand anywhere near the multitrillion-dollar value levels of gold, bonds, and stocks. Investors looking for stable assets would clearly be better served to put their money into any of the three larger asset classes, not to mention alternatives such as real estate or owning your own business.

On the flip side, let’s imagine a future where bitcoin (or some better-designed cryptocurrency) becomes a viable alternative to owning gold and reaches a similar market scale. If it’s bitcoin, that would require its value to increase at least 40-fold from current levels. We’re not likely to see a surge like that in a single upward run; bitcoin only multiplied 21-fold during its historic price run of 2017, and the volatility of investments tends to fall as the assets grow larger.

But many investors/speculators/visionaries/gamblers (pick your preferred epithet) are betting on that bullish outcome in this all-or-nothing asset class. Over a recent 24-hour period, $46 billion of bitcoin tokens changed hands, or 25% of the entire currency. That’s huge next to the average daily dollar volumes of trading in Adobe ($734 million) or scandal-stricken Boeing ($2.15 billion). It’s even enormous in comparison to trillion-dollar market behemoth Apple, whose average dollar volume clocks in at $8.8 billion.

It takes a lot of traders to move that much bitcoin in a single day, including plenty of deep-pocketed market makers. Bitcoin’s trading volumes have never been this overheated, not even at the peak of 2017’s crypto-mania, when daily trading topped out near $23 billion.

I wouldn’t be surprised to see bitcoin and friends making a big move soon as the higher trading pressure either becomes the new normal or pops and drops. Whether the cryptocurrency market rises or falls, I’m content to simply hold on to my tiny crypto portfolio, which consists of a $20 “let’s try this” whim from six years ago.

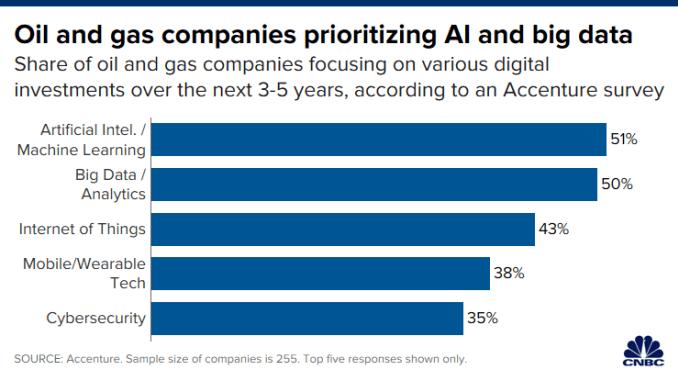

As the energy industry faces a time of reckoning — pressured by consistently low oil prices, high operating costs and a growing sustainable investing movement — oil and gas companies are increasingly turning to Silicon Valley for help streamlining operations and boosting efficiencies.

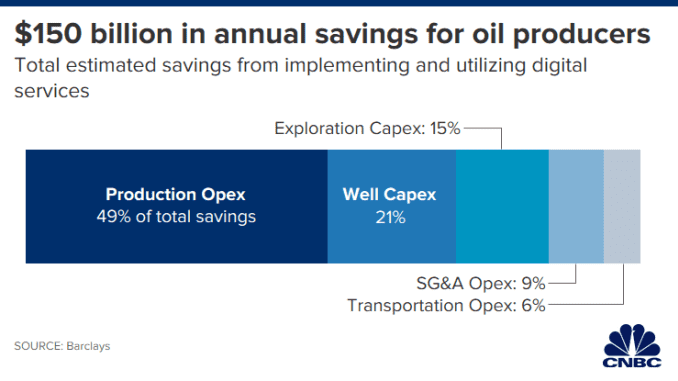

By some estimates, the addressable market for digital oil and gas solutions could grow 500% over the next five to six years, saving oil producers roughly $150 billion, while creating an ever-larger market for tech companies in the highly competitive — and high margin — business of cloud computing.

Opportunities for savings include cutting capital expenditures as well as selling, general and administrative operating costs and transportation operating costs.

“The digital age is finally dawning for Oil & Gas … We see a market poised to erupt over the next five years,” Barclays said in January in a note to clients. “The last 12 months has seen a dramatic shift in adoption, with numerous announcements of cloud and digital-platform partnerships that we think are just early signs of things to come,” the firm added.

In the last year, Microsoft has announced partnerships with Exxon and Chevron, among others, while in May Google parent company Alphabet renewed and significantly expanded its partnership with Schlumberger. Amazon Web Services offers digital services to the industry through its oil and gas division, and counts BP and Shell among its clients.

Energy giants have, of course, been using tech companies’ enterprise software for years, and oil and gas companies’ highly complex operating systems — including precise drilling techniques and rig management operations — have depended on sophisticated data-based decision making for decades.

But oil companies were traditionally somewhat reluctant to hand over their treasure troves of valuable data thanks to cyber security concerns and wanting to maintain competitive advantages, among other things. This meant that for the most part software was developed in-house or by companies within the oilfield services sector.

Now, however, driven by lackluster returns in the energy space and rapid advancements in the tech sector, the two sectors are increasingly coming together, creating partnerships between two industries that in other ways are very much at odds with one another.

“The magnitude of the capacity for processing and storage makes it possible to do things we didn’t dream of within the industry,” said John Gibson, Flotek chairman and CEO and former chairman of energy technologies for energy investment bank Tudor, Pickering, Holt & Co.

“The whole industry needs an uplift in performance, profitability and free cash flow, so working together with the data to improve industry performance has become a mandate … We need the tide to rise for everybody,” he added.

Why now?

A number of factors are driving the transition, including years of lagging returns in the energy sector.

As recently as six years ago, when oil fetched more than $100 per barrel, producers’ costs weren’t looked at under a microscope. U.S. West Texas Intermediate began a downward trajectory in 2014 and while prices have rebounded from the extreme lows of 2016, WTI remains far from its prior highs, meaning oil and gas companies have had to adapt.

“The oil business here [North America] has gone from gold rush to austerity in a very short period of time,” Shaia Hosseinzadeh, founder of energy-focused private equity firm OnyxPoint Global Management, said. “In this new world, there are a lot of demands being placed on the oil industry. … The entire ecosystem is being asked to do more with less.”

Energy’s continued underperformance — it now accounts for less than 4% of the S&P 500, compared to more than 11% in 2010 — has coincided with major advancements in the tech space, including rapid iterations in areas like machine learning and data processing. At the same time, widescale adoption has led to steep cost declines for things like data storage.

Tech companies can harness insights from applications refined and tested across sectors. It’s difficult — if not impossible — for individual companies to fully replicate what they offer. In other words, partnerships where applications and technologies are co-developed can be the only choice.

“They [energy companies] are realizing that they’re not IT companies. They’re not software developers, but they are users of it,” IHS Markit director Carolyn Seto said to CNBC. “They are partnering with these [tech] companies to be able to gain access to these new technologies, as opposed to taking the development costs themselves of building out capabilities within their organization.”

Reid Morrison, oil and gas advisory leader at PwC, noted that as oil prices rebounded from 2016 lows it also created an opportunity for energy companies to advance these technologies from proof-of-concept to actually moving them into the mainstream where they can hit the companies’ bottom line.

Barclays also made this point, noting that “value creation over the next five years hinges on scalability as Digital moves beyond discrete applications to organization-wide implementation.”

Biggest beneficiaries

As big oil looks to data services and cloud computing to help its performance and profitability, companies that provide these services could be in for a big payday.

Barclays estimates that the digital services market could grow to $30 billion annually over the next five years, from less than $5 billion today, with the potential market for cloud providers also growing to $30 billion annually. Given the potential size, tech companies are vying for market share.

Raymond James analyst Pavel Molchanov said in a 2019 note to clients that while the cost savings might not be all that pronounced for energy companies, “the sale of these products and services – to energy and other verticals, taken in aggregate — can be quite needle-moving for technology providers.”

“There is an enormous opportunity to bring the latest cloud and AI technology to the energy sector and accelerate the industry’s digital transformation,” Microsoft CEO Satya Nadella said in a statement in June while announcing the company’s three-party collaboration with Schlumberger and Chevron.

On the energy side, Barclays estimates that greater efficiencies will save producers roughly $150 billion annually, which translates to shaving $3 per barrel from the production price of oil.

Besides the oil producers themselves, Barclays said there’s a “golden opportunity” for oilfield services companies like Schlumberger, Halliburton and Baker Hughes to “regain relevancy.” These companies have deep industry experience, and also have their own digital offerings.

The firm said that in the near-term Schlumberger is best-positioned, but that Baker Hughes “may have the greatest upside of all.” The firm noted that these numbers are just estimates since it’s difficult to quantify given the secrecy surrounding the field.

Longer term, technological advancements will also be a way for energy companies to stand out in a cutthroat industry, said Rebecca Fitz, senior director at BCG’s Center for Energy Impact. “In an unhelpful oil price environment, companies could competitively differentiate themselves by growing their margins more than their peers. And that’s where technology becomes interesting.”

The ESG factor

For obvious reasons, oil and gas companies are particularly vulnerable to the growing ESG movement, which is when environmental, social and governance factors are prioritized when making investing decisions. Against this backdrop, energy giants are leaning on tech companies to help them make operations cleaner and safer.

Remotely monitoring operations can help companies quickly identify leaks and therefore mitigate the environmental impact, for example. This also means that fewer personnel are exposed to dangerous conditions. Additionally, the very act of moving data to the cloud means that oil and gas companies can reduce the number of energy-intensive data centers needed.

If tech’s involvement helps to boost energy companies’ ESG ratings, it could come at the expense of the tech companies’ ratings. Some argue that since the world is still dependent on fossil fuels, tech companies should help oil and gas companies be as energy-efficient as possible. Others say that making the industry more cost-effective will delay the widespread adoption of renewable energy. When Exxon and Microsoft announced their partnership last February, the oil giant said it could lead to an additional 50,000 oil-equivalent barrels of production per day in the Permian by 2025, generating “billions of dollars in value over the next decade.”

Amazon and Microsoft have recently unveiled ambitious plans to become carbon neutral and carbon negative, respectively, and relying on power generated from renewable sources is just one of the ways in which they’ve sought to make their operations more environmentally friendly.

But still, the tech companies have faced backlash — most notably, perhaps, from employees — for their involvement in the oil and gas industry.

What happens next?

Despite the changes in the last few years, Barclays said that this trend is still in its infancy, although acknowledged that the market can be difficult to gauge due to the secretive nature of oil and gas companies.

But after looking at the sector for many months, the firm said this change in enabling technologies looks set to accelerate.

“Our research reveals a much more vibrant, complex and opportunistic digital oil & gas market than most investors realize; one that is just now starting to emerge,” the firm said.