Stock Markets

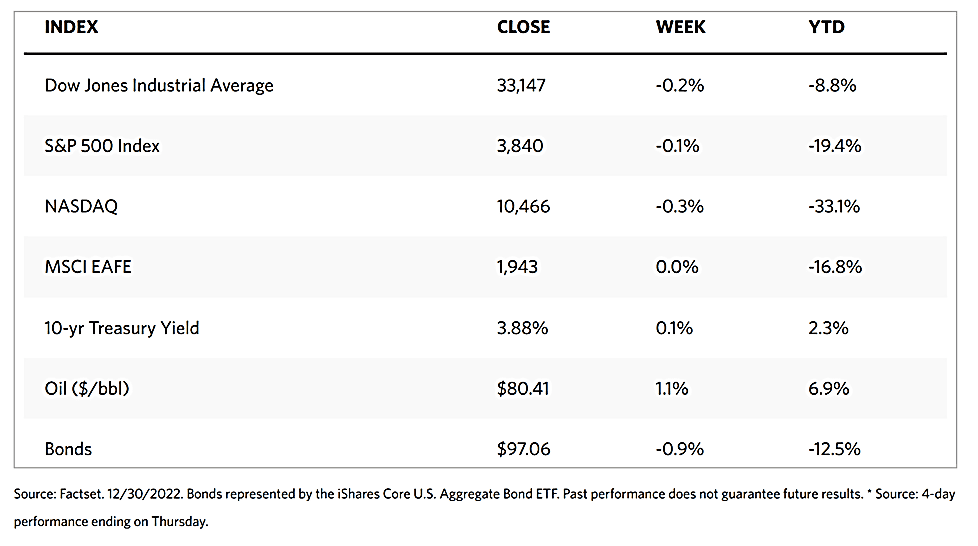

Stocks closed the year down on thin trading volumes ahead of the long New Year’s holiday weekend. The Dow Jones Industrial Average (DJIA) is down for the week by 0.17%, while the total stock market index lost 0.09%. The S&P 500 Index slid by 0.14% while the Nasdaq Stock Market Composite fell by 0.30%. The NYSE Composite Index lost 0.03% of its value. CBOE Volatility rose by 3.83%, indicating that investors perceive greater risk during the week’s trading. The S&P 500 Index remained above its intraday low seen the week before. Underperforming the most were consumer staples and materials shares. Thanks in large part to the strength of Target and several other retailers, consumer discretionary shares were resilient. Shares of Southwest Airlines plummeted when trading opened on Tuesday due to a highly publicized wave of flight cancellations. However, the airline recovered some ground for the remainder of the week. Bond trading closed early on Friday ahead of the holidays, and both equity and bond markets are scheduled to be closed on Monday in observance of New Year’s Day.

U.S. Economy

There were few economic reports released during the week to provide much impetus for strong market movement. As expected, many investors remained sidelined as a prudent move before the start of 2023. Investors and analysts are keeping a close watch on the global impact of China’s relaxation of COVID containment rules even as the data shows that concerns of rising infection rates might usher back loosened pandemic restrictions.

Despite the relatively little data that came out during the week, these were suggestive of improving economic conditions. The Richmond Fed’s index of manufacturing activity in the Mid-Atlantic region recorded its first positive reading in eight months, which indeed ushered in the good news. Wages continued to increase at a solid pace in December. Supply chains also eased, suggesting lower prices paid and received, suggesting that inflation expectations for the coming year may be much lower than current price trends. Weekly jobless claims increased from 215,000 to 225,000, which is still in line with expectations and below their mid-November peak of 241,000.

Metals and Mining

Gold and silver prices remain largely unchanged in quiet early U.S. trading this week. A possible explanation for the light volumes and thin conditions is that many traders are already on holiday during the week. For the year, the gold market had a solid end to 2022 and its momentum in the fourth quarter should continue into 2023. Analysts see gold prices pushing above $1,900 per ounce next year, with the positive outlook encouraging some firms which had been building a bullish position starting November this year. The Federal Reserve’s monetary policy is expected to peak while persistently high inflation and global economic uncertainty may incentivize support for safe-haven assets such as gold through the new year. There may likewise be increased physical demand driven by central bank purchases.

This past week, spot prices for precious metals climbed to end the week marginally up. Gold rose by 1.44%, from the week-ago close at $1,798.20 to this week’s price at $1,824.02 per troy ounce. Silver came from its previous price of $23.73 to this week’s price of $23.95 per troy ounce for an increase of 0.93%. Platinum ended this week at $1,074.29 per troy ounce, which is 4.60% above the previous week’s price of $1,027.01. Palladium closed one week ago at $1,754.28 and this week at $1,792.68 for a price increment of 2.19%. The three-month LME prices of base metals were also slightly up for the week. Copper ended the week at $8,418.00 per metric tonne, 0.82% higher than its closing price the previous week at $8,349.50. Zinc went from last week’s price of $2,965.00 to this week’s close at $2,984.50 per metric tonne, up by 0.66%. Aluminum ended this week at $2,405.00 per metric tonne, up by 0.65% from the previous week’s price of $2,389.50. Tin, which closed the week before at $23,934.00, ended this past week at $24,915.00 per metric tonne for a gain of 4.10%.

Energy and Oil

A large number of gas-producing basins have reduced production by as much as 30% due to periods of extremely cold weather. Top among them was the Appalachian Basin, which will likely take several weeks to rebound to pre-freeze levels. Given that U.S. production seasonally dips in the new year, the worst-case scenario is that it may take months before production recovery returns to normal levels. On a more positive note, refiners on the U.S. Gulf Coast may resume operation at a dozen facilities where production was halted due to the recent freeze. This involves a total operable capacity of 3.6 million barrels per day, with Deer Park and Port Arthur taking at least one to two weeks before they fully return.

Natural Gas

U.S. LNG developer NextDecade announced that it will increase the volume of liquefied natural gas provided under a term agreement with China’s ENN Natural Gas, from 0.5 million tons per annum (mtpa) to 2 mtpa, to be sourced from the upcoming RGLNG Project. In other news, the U.S. LNG company Excelerate Energy has delivered Finland’s first-ever floating storage and regasification unit (FSRU) Exemplar, rated at 5 billion cubic meters (bcm) per year capacity. It was delivered to the port of, Inkoo, one of the 19 new FSRU projects to be commissioned over the next few years in Europe.

World Markets

Equities pulled back in European stock markets, not surprisingly during a week of thin trading ahead of the New Year’s holiday weekend. The pan-European STOXX Europe 600 Index slid by 0.60% over the five trading days ending on December 30. France’s CAC 40 Index lost by 0.48% while Italy’s FTSE MIB Index dipped by 0.71%. Germany’s DAX Index came down modestly. The UK’s FTSE 100 Index declined by 0.28%. Members of the European Central Bank’s (ECB) Governing Council expressed sentiments that there may be additional monetary policy tightening in the next five policy meetings. There was a possibility of continued half-percentage point increases in response to further inflation rate increases. Any recession was expected to be short and shallow, as the recent economic data of some eurozone countries like Germany were already showing signs that the worst was already behind them.

Japanese equities were positive at the start of the final trading week for the year, recording early gains despite thin trading volumes. By Thursday, the Nikkei 225 fell to three-month lows only to claw back some of its lost ground on Friday. The index ended down by 0.54% for the week and also down by 9.37% for the year. This is the Nikkei’s first annual loss in four years. In currencies, the yen rebounded in late-week trading after the Bank of Japan (BoJ) announced a series of unscheduled bond purchases. The markets found some encouragement in signs that the U.S. inflation rate may be coming down, as well as from comments from BoJ Governor Haruhiko Kuroda that the central bank does not intend to change its customary easy monetary policy stance. Additional optimism came from China’s announcement that it would drop quarantine requirements for international arrivals starting January 8, which is seen as a first step towards reopening its borders.

China’s stock market rose in response to Beijing’s continued easing of coronavirus pandemic restrictions, despite a surge in cases. The Shanghai Composite Index climbed by 1.42% and the blue-chip CSI 300 gained 1.13%, seen as a reversal of several weeks of losses. In Hong Kong, the benchmark Hang Seng Index ascended by 1.61%. Regarding the country’s coronavirus status, the National Health Commission (NHC), the country’s health regulator, downgraded the management of the pandemic response from the highest to the second-highest level starting January 8, 2023. The focus will remain on vaccinating the elderly, ensuring medical supply availability, and tiered medical treatment. Almost all standard restrictions, however, will be lifted, according to a statement b the NHC over state-run media. In other news, economic activity picked up across several cities in China where COVID-19 virus cases have shown signs of peaking. Reports showed that traffic congestion, movie sales, and air travel have increased in some areas.

The Week Ahead

Among the important economic news expected to be released in the coming week are job openings, jobless claims, trade deficit, and construction spending.

Key Topics to Watch

- S&P U.S. manufacturing PMI (final)

- Construction spending

- ISM manufacturing index

- Job openings

- Quits

- FOMC minutes

- Motor vehicle sales (SAAR)

- ADP employment report

- Initial jobless claims

- Continuing jobless claims

- Trade deficit

- S&P U.S. services PMI (final)

- Nonfarm payrolls

- Unemployment rate

- Average hourly earnings

- Labor force participation rate, ages 25-54

- ISM services index

- Factory orders

- Core equipment orders

Markets Index Wrap Up