Stock Markets

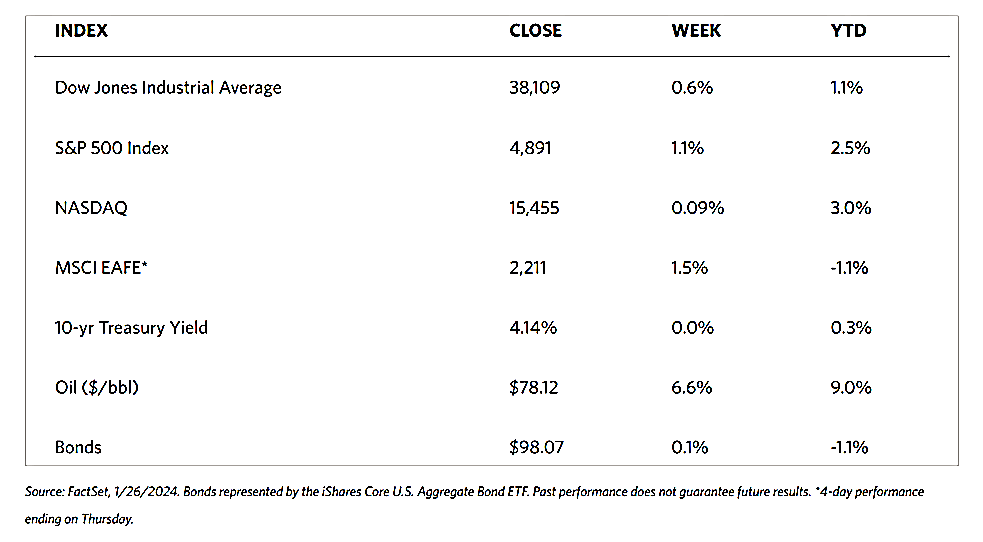

It was a week of gains for stocks, albeit moderate. The Dow Jones Industrial Average (DJIA) modestly rose by 0.65% while the DJ Total Stock Market Index rose by a heftier 1.08% although utilities underperformed the other sectors, slipping by 0.32%. The broader S&P 500 Index closely mirrored the Total Stock Market, advancing by 1.06%. The technology-heavy Nasdaq Stock Market Composite gained by 0.94% and the NYSE Composite climbed by 1.31% with all Russell Indexes up. The CBOE Volatility Index (VIX), an indicator of investor risk perception, moved slightly downward by 0.30%.

The DJIA and the S&P 500 climbed to new all-time highs; for the latter, this marked the 12th weekly advance out of the last 13 weeks. Overall gains were modest but relatively broad. The small-cap Russell 2000 Index remained almost 20% below its all-time intraday high. Investors’ attention focused on the growing stream of fourth-quarter earnings reports this week, given the lack of comments or speeches by Federal Reserve Officials ahead of the upcoming policy meeting. Included among the stocks that moved the market was Tesla, which plunged sharply after it missed both earnings and revenue estimates. Tesla also warned of slower growth in 2024. On the other hand, Netflix charted solid gains attributable to an unexpected increase in subscribers.

U.S. Economy

Over the week, the economic calendar was light, although two economic reports revealed data that continue to support the argument for a soft landing in the U.S. First, the S&P PMI data for both services and manufacturing indicated that these sectors were expanding in January, if barely. Second, fourth-quarter GDP growth came in at 3.3% and exceeded analysts’ expectations of a 2.0% growth rate. These data may be backward-looking, however, they continue to solidify the upward economic trend and confirm that the U.S. economy was not softening as the new year began. On the contrary, economic growth was seen to accelerate at the end of 2023. Furthermore, inflation showed signs of moderation at the same time the economy was strengthening.

Other developments worth mentioning include the 0.3% increase in December in the orders for nondefense capital goods excluding aircraft, which is widely considered as a proxy for business investment. The economy grew by 2.5% over the year as a whole, an increase from the 2022 growth rate of 1.9%. The core personal consumption expenditure (PCE) price index, which is the Fed’s preferred inflation metric, advanced by 2.0% year-on-year in the fourth quarter, in line with expectations and the Fed’s long-term target. Financial markets should be broadly supported by the “Goldilocks” outcome, referring to the better-than-expected growth simultaneous with easing inflation. Some downward pressure on interest rates should be evident at this point.

Metals and Mining

Gold investors face a challenging environment with the Federal Reserve continuing to chart a course that makes it difficult for the precious metal to gain bullish momentum. The most recent economic data suggests that while falling inflation may provide the Fed room to cut interest rates, the general economic health does not require them to. Gold is struggling to maintain its current levels, partly due to the report by the U.S. Commerce Department that personal consumption increased by 0.7% in December, significantly higher than expected. This confirms the trend suggested by previous data that retail sales activity was robust during the holiday season. However, one worrying aspect of the recent economic growth trend is that it is mostly funded by debt, bolstered by buy-now-pay-later schemes. This is unsustainable. Economists and analysts note that this is the final stage of consumption because consumers have burned through their earnings and inflation continues to erode their purchasing power. The value of holding safe-haven assets such as gold and silver may presently elude most investors, however, for those who are patient, these are the times that present the best opportunities.

The spot prices of precious metals were mixed for the week. Gold lost by 0.54%, dipping from its previous weekly close at $2,029.49 to this week’s close at $2,018.52 per troy ounce. Silver, on the other hand, rose by 0.80%, bringing its weekly close from last week’s $22.62 to this week’s $22.80 per troy ounce. Platinum gained by 1.37% from last week’s closing price of $903.27 to this week’s closing price of $915.68 per troy ounce. Palladium also gained, closing 1.02% higher from last week’s closing price of $950.61 to end this week at $960.31 per troy ounce. The three-month LME prices for base metals were generally up for the week. Copper gained by 2.60%, from the previous week’s price of $8,351.00 to this week’s price of $8,568.50 per metric ton. Zinc climbed by 4.79%, from its previous weekly close at $2,462.00 to the recent week’s close at $2,580.00 per metric ton. Aluminum realized a 3.35% gain, from last week’s close at $2,166.00 to this week’s close at $2,238.50 per metric ton. Tin advanced by 5.34% from last week’s close at $25,298.00 to end this week at $26,648.00 per metric ton.

Energy and Oil

Oil prices were boosted this week to their highest level for the year by the release of stronger-than-expected performance in the U.S. economy. The announcement of a 3.3% GDP growth for the fourth quarter surprised many analysts and investors. The bullish cause gained added momentum as a result of continuous Houthi strikes in the Red Sea and surging product freight rates. The White House has asked for China’s help to rein in the Houthi rebels attacking commercial tankers plying the Red Sea after two Maersk container ships were targeted this week despite the presence of U.S. warship escorts. China has been reaching out to Iran in an attempt to prevent further Yemeni attacks, but this has failed to ease geopolitical tensions. This week, Brent broke through the $80 per barrel threshold and reached $82 per barrel, which is sufficient for a major psychological price barrier to be overcome. This is a technical signal that oil prices may be expected to reach higher levels.

Natural Gas

For the report week that began Wednesday, January 17, and ended Wednesday, January 24, 2024, the Henry Hub spot price fell by $0.43 from $2.87 per million British thermal units (MMBtu) to $2.44/MMBtu. Regarding Henry Hub futures, the price of the February 2024 NYMEX contract decreased by $0.229, from $2.870/MMBtu at the beginning of the week to $2.641/MMBtu by the end of the report week. The price of the 12-month strip averaging February 2024 through January 2025 futures contracts declined by $0.145 to $2.815/MMBtu. International natural gas futures decreased this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia fell by $1.01 to a weekly average of $9.49/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, decreased by $0.71 to a weekly average of $8.92/MMBtu. In the week last year that corresponds to this report week (the week from January 18 to January 25, 2023), the prices were $22.42/MMBtu and $19.67 /MMBtu in East Asia and at the TTF, respectively.

World Markets

The pan-European STOXX Europe 600 Index closed the week higher by 3.11% on the back of encouraging corporate results and announcement of additional stimulus measures by China. Also contributing to improved market sentiment was the dovish outlook signaled by the European Central Bank (ECB) by leaving interest rates unchanged. Most major indexes in the region climbed. France’s CAC 40 Index surged by 3.56%, Germany’s DAX jumped by 2.45%, and Italy’s FTSE MIB advanced by 0.32%. The FTSE 100 Index of the U.K. climbed by 2.32%. Simultaneously, the European government bond yields declined. The yield on the benchmark 10-year German bond dipped as did the French and Swiss sovereign bonds of the same maturity. The ECB retained its key interest rates at the same level at record highs and repeated that it would continue to enforce its strict monetary policy “at sufficiently restrictive levels for as long as necessary” to bring inflation under control until it reaches the 2% target. The central bank stressed, however, that policy decisions would continue to be guided by economic and financial data as they develop.

Japanese equities declined this week. The Nikkei 225 Index fell by 0.6% while the broader TOPIX Index dropped by 0.5%. The Bank of Japan (BoJ) retained its ultra-accommodative stance and its forward guidance. However, Governor Kazuo Ueda emphasized the BoJ’s progress toward achieving sustained inflation, which raised expectations that a monetary policy shift is within sight. These hopes were somewhat tempered later in the week by a softer-than-forecasted Tokyo area inflation reading, a leading indicator for nationwide price trends. Influenced by ongoing speculation regarding the impending end of Japan’s negative interest rate policy, the yield on the 10-year Japanese government bond (JGB) rose to 0.71% from 0.66% at the end of the week previous. The yen strengthened to the high JPY 147 range from about JPY 148 the week before.

Chinese stocks rose after Beijing announced the implementation of forceful stimulus measures in support of the economy. The Shanghai Composite Index advanced by 2.75% while the blue-chip CSI 300 Index rose by 1.96%. The Hong Kong benchmark Hang Seng Index surged by 4.2%. The People’s Bank of China (PBOC) announced a cut in its reserve ratio requirement (RRR) by 0.50% or 50 basis points for most banks. The RRR cut will take effect on February 5 and shall mark the first cut in banks’ reserve this year. The bank also announced that it will lower interest rates by 0.25% or 25 basis points for refinancing and rediscounting beginning January 25, to support agriculture and small businesses. In 2023, the PBOC cut the RRR twice, the last cut being in September. After the PBOC kept its medium-term lending rates unchanged the week prior, Chinese banks maintained their one- and five-year loan prime rates at current rates, as expected. In other developments, regulators lifted the draft rules imposed on online games in late December, aimed at curbing spending and rewards. When they were first announced, the regulations eliminated almost US$80 billion in market value from some of China’s largest gaming companies due to investors fearing the likelihood of another crackdown on the sector.

The Week Ahead

Among the important economic data expected to be released this week are the results of the FOMC meeting and labor market data (nonfarm payrolls report, unemployment rate, and hourly wages for January).

Key Topics to Watch

- S&P Case-Shiller home price index (20 cities) for November

- Job openings for December

- Consumer confidence for January

- ADP employment for January

- Employment Cost Index for the Fourth Quarter

- Chicago Business Barometer (PMI) for January

- Fed interest rate decision

- Initial jobless claims for Jan. 27

- U.S. Productivity for the Fourth Quarter

- S&P U.S. manufacturing PMI (final) for January

- ISM manufacturing

- U.S. nonfarm payrolls for January

- U.S. unemployment rate for January

- U.S. hourly wages for January

- Hourly wages year-over-year

- Factory orders for December

- Consumer sentiment (final) for January

Markets Index Wrap-Up