Stock Markets

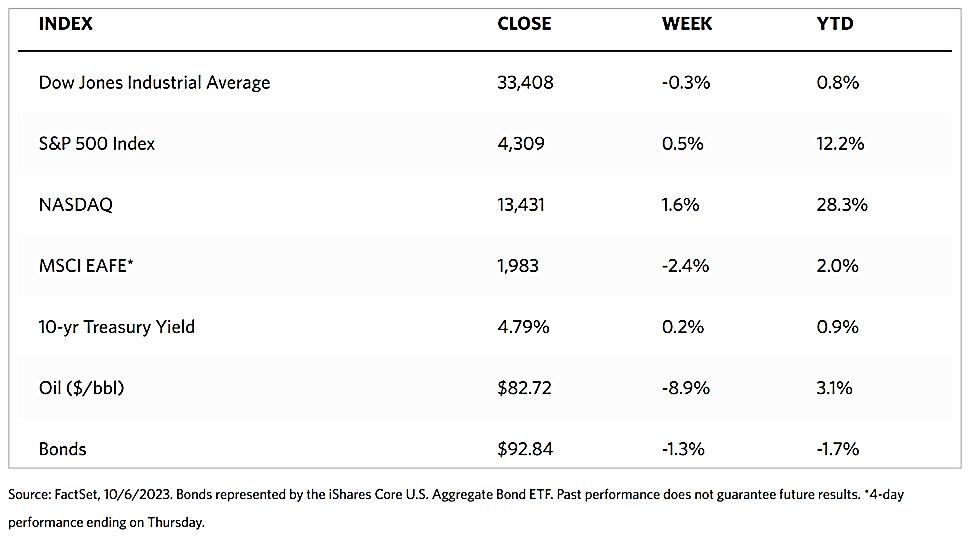

Another week of directionless trading ended in mixed major indexes. The Dow Jones Industrial Average (DJIA) closed down by 0.30% over the week while its Total Stock Market counterpart ended up by 0.19%. The broad-based S&P 500 Index was slightly up by 0.48% while the midcap and small-cap stocks were down by 1.87% and 2.37%, respectively. The technology-heavy Nasdaq Stock Market Composite was up by 1.60%, while the NYSE Composite Index was down by 1.20%. The risk perception indicator, CBOE Volatility Index (VIX) ended the week lower by 0.40%.

During the week, the mega-cap information technology and internet stocks which constitute the bulk of the large-cap growth stocks outperformed the rest of the market. The Russel Index also showed how large caps outpaced the small-caps by the widest margin since March. Volumes were muted for most of the week as investors sought confirmation from economic indicators regarding the market’s direction. Investors were hoping that the official nonfarm payrolls report, due for release on Friday, would show another decline in hiring. This development was expected to convince the Federal Reserve to forego another rate hike in their monetary policy as such would be a welcome sign of cooling inflation. Before the equity market opened, however, stocks fell sharply on the news that more than double the expected new jobs created was reported by the Labor Department, suggesting that the economy was heating up and, therefore, inflation may be on the rise again.

U.S. Economy

The Labor Department reported an additional 336,000 nonfarm jobs added in September, a number double the consensus estimate and an acceleration from the previous three-month-average of 190,000. The closely watched official nonfarm payrolls report revealed that the average hourly earnings rose by 0.2% in the month, pulling the year-over-year gain down to 4.2%, the lowest level it has been since June 2021. The workforce participation rate likewise remained at the best level it has been since the beginning of the pandemic lockdowns in February 2020, at 62.8%.

The figures indicated a more nuanced bigger picture, that increasing supply was driving the labor market rather than a rampant demand for workers, thus reflecting a more benign inflationary environment. The unemployment rate held steady at 3.8%, accompanied by a growing number of workers joining the workforce. The ongoing health of the labor market is viewed as categorically positive for consumers and GDP growth. Unfortunately, the market is seeing it through the lens of the upcoming Fed monetary policy as a reason for the policymaking body to hike rates. This caused yields to move up and stocks to pull back.

Metals and Mining

After seeing nine consecutive months of losses, the gold market did not start the fourth quarter with a good performance, continuing the precious metal’s longest daily losing streak in seven years. The yellow metal still ended this week with an almost 1% loss, although its closing price was still off its seven-month lows. As it looks to hold critical near-term support levels, there is still hope for gold, even though it will continue to be sensitive to rising bond yields. The U.S. bond market saw a significant selloff in long bonds while gold was treading its March lows, thus driving yields higher. The 30-year yield rose to 5% this week for the first time since 2007. Simultaneously, the yield on 10-year notes rose to a new 16-year high at 4.8%.

The spot prices for precious metals closed lower for the week. Gold closed at $1,833.01 per troy ounce this week, down by 0.84% from last week’s close at $1,848.63. Silver closed at $21.60 per troy ounce this week, down by 2.61% from the previous week’s close at $22.18. Platinum ended the week at $881.56 per troy ounce, down by 2.90% from last week’s close at $907.90. Palladium closed this week at $1,162.78 per troy ounce, 6.84% down from last week’s close at $1,248.19. The three-month LME prices of industrial metals were generally down for the week. Copper, which ended the previous week at $8,270.50, closed this week at $8,046.00 per metric ton, down by 2.71%. Zinc, which closed one week ago at $2,649.50, ended this week at $2,509.00 per metric ton, down by 5.30%. Aluminum, which ended last week at $2,347.00, closed this week at $2,239.50 per metric ton, down by 4.58%. Bucking the trend is Tin, which rose by 2.92% from its previous close at $23,944.00 to its close this week at $24,644.00 per metric ton.

Energy and Oil

The week just ended was the worst week for crude since March. Pressured by the U.S. bond selloff that cast a shadow over the economic outlook for 2024, oil prices have receded by $10 per barrel. This week’s EIA numbers indicated a steep drop in gasoline demand across the U.S., thus dealing another blow to crude prices. On the supply side, Saudi Arabia announced that it is maintaining its 1 million barrel per day production cut until the end of the year 2023 and signaled it would review its decision again next month and deepen the cut if required. With focus directed at the U.S. non-farm payroll data released on Friday, the chances of ICE Brent, currently hovering at $84 per barrel, climbing to triple digits is firmly out of the question for now.

Natural Gas

For the report week beginning Wednesday, September 27, and ending Wednesday, October 4, 2023, the Henry Hub spot price rose by $0.20 from $2.71 per million British thermal units (MMBtu) to $2.91/MMBtu. The October 2023 NYMEX contract expired on October 4 at $2.764/MMBtu. The November 2023 NYMEX contract price increased to $2.962/MMBtu, up by $0.06 from the start to the end of the report week. The price of the 12-month strip averaging November 2023 through October 2024 futures contracts rose by $0.04 to $3.260/MMBtu.

International natural gas futures prices were mixed for this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia increased by $0.20 to a weekly average of $14.44/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, decreased by $0.50 to a weekly average of $12.11/MMBtu. In the week last year corresponding to this week (the week beginning September 28 and ending October 5, 2022), the prices were $37.99/MMBtu and $51.00/MMBtu in East Asia and at the TTF, respectively. Stocks of natural gas in storage in the European Union reached 96.3% of capacity on Tuesday, compared with 89.7% on the same day last year.

World Markets

In reaction to the surge in bond yields amid worries about an extended period of higher interest rates, the pan-European STOXX Europe 600 Index ended lower by 1.18% in local currency terms. The major stock indexes likewise lost ground. Germany’s DAX fell by 1.02%, France’s CAC 40 Index dipped by 1.05%, and Italy’s FTSE MIB plunged by 1.53%. The UK’s FTSE 100 Index fell by 1.49%. At the end of a volatile week in the European bond markets, the yield on Germany’s 10-year government bond fell below 3% but remained near its highest in more than a decade. Amid cautious sentiment, French and Italian bond yields ticked up. In the UK, the yield on the benchmark 10-year UK government bond stayed close to its highest levels going all the way back to August 2008 on signs of sticky inflationary pressures.

In Japan, stocks fell over the week. The Nikkei 225 Index came down by 2.7% while the broader TOPIX Index slid by 2.6%. Amid surging U.S. bond yields and concerns that central banks will remain defensive for a longer period, Japanese equities came under pressure. The country’s economic data signaled that real wages and consumer spending continued to plummet in August, thus further weighing on investor sentiment. On the contrary, business sentiment among Japanese companies was boosted by a weak yen, as shown by the Bank of Japan’s (BoJ’s) latest quarterly Tankan survey, thus lending some support to equities. There was widespread speculation that Japan’s Ministry of Finance (MoF) intervened in the foreign exchange market to arrest the freefall of the yen, following the currency’s almost instantaneous surge after it breached the JPY 150 level versus the U.S. dollar. Many participants anticipated that this breach could serve as a trigger for monetary authorities to take action. After the yen fell to its lowest level in 11 months, the MoF officials neither confirmed nor denied whether they intervened. However, they continued to stress that they would act to control excess volatility without ruling out any options. The yen closed the week stronger at around JPY 149 against the greenback.

China’s financial markets were closed this week in celebration of the Mid-Autumn Festival and National Day holiday. They are scheduled to reopen on Monday, October 9. The Hong Kong benchmark Hang Seng Index declined by 0.14% for the holiday-shortened weekend. On the economic front, China’s factor activity entered into expansion territory for the first time since March, the most recent indication that the economy may have at last bottomed out. The official manufacturing PMI rose to 50.2 in September, an optimistic outcome since above 50 signals expansion, and the reading was better than expected as well as higher than the 49.7 reading for August. The nonmanufacturing PMI was also higher than consensus, at 51.7 in September from 51.0 in August. A separate indicator, the private Caixin/S&P Global survey of manufacturing and services activity both came down slightly from the previous month although they remain in expansion. During the eight-day holiday, domestic activity in China picked up significantly. During the first four days of the holiday, about 395 million trips were taken by road, rail, air, and waterways which reckoned as 76% higher than the same period the previous year. Box office sales reached RMB 1.2 billion in the first three days, also higher than corresponding sales last year. The offshore gambling hub of Macau recorded more than 160,000 visitors from mainland China and Hong Kong on Saturday, the highest single-day total since the pandemic.

The Week Ahead

Among the important economic news scheduled for release this week are the minutes of the Federal Reserve’s September FOMC meeting, the consumer price index (CPI), and producer price index (PPI) inflation data.

Key Topics to Watch

- Dallas Fed President Logan speaks

- Fed Gov. Jefferson speaks

- KFIB optimism index for September

- Wholesale inventories for August

- Producer price index for September

- Core PPI for September

- PPI year over year

- Core PPI year over year

- Minutes of Fed’s September FOMC meeting

- Initial jobless claims for October 7, 2023

- Consumer price index for September

- Core CPI for September

- CPI year over year

- Core CPI year over year

- Import price index for September

- Import price index minus fuel for September

- Consumer sentiment (preliminary) for October

Markets Index Wrap-Up