With the current market environment it can be tough to know what companies to look at when it comes to investing. We have been waiting for an opportune time to put our research to work, and now we believe the markets in this sector have evolved to a point where we can start giving you some information to base your research on. If you are interested in hearing more about this sector, simply enter your email in the box provided and we will send you our information as it becomes available. Thank you

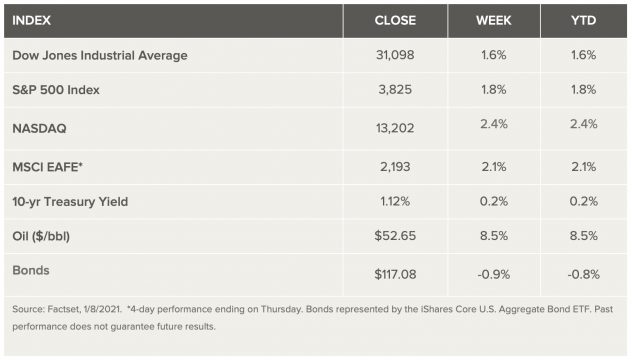

World stock markets saw strong gains as major indices broke records during the first week of trading for the year. Following the two runoff elections in Georgia, Democrats gained the majority in the Senate that may signal further fiscal stimulus later in the year to push economic recovery. An increase in corporate tax rates is a possibility as a result of Democrat control of the government, although this may not be a priority for 2021 due to the tenuous economic recovery and the party’s slim majority. For the first time in nine months, ten-year yields rose above 1%, and anticipation of strong performance in the post-vaccine phase caused small-cap and international stocks to outperform. The positive sentiment was bolstered by the return of WTI oil prices to February levels, rising above $50 in response to announcements of an expected production cut by Saudi Arabia.

U.S. Economy

Over the past week, economic data showed a combination of resiliency and lockdown stress. Political uncertainties dominated the news, and expectations of a policy stimulus and post-vaccine recovery pushed stock market activity. The optimism surrounding the economy’s strong underlying fundamentals, expectation of corporate profits, and stable interest rates fueled the stock gains and signaled investors’ bright outlook in the long-term.

The market performed well over the past year, posting a 10% average return. Considering that this is a presidential election year, the market gains are encouraging.

A Democratic White House and Congress are expected to push for fiscal stimulus through increased aid for households and increased government spending that may include an infrastructure bill. These measures are expected to boost the economy despite an increase in public debt.

The 34% market plunge that occurred in 2020 as a result of the pandemic lockdowns is an aberration that quickly recovered with a 60% rally in the past five months. A new bull market has most likely begun, sustained by increasing corporate earnings and low interest rates that will continue to give rise to a strong domestic and global economy.

The bottom line is that we are likely seeing the early stage of a new economic expansion. Pressures from pandemic protocols and the resulting constraints on business activity may cause temporary stalls such as the loss of 140,000 jobs in December, the first monthly loss since April. However, these are expected to give way to a sustained new normal for the rest of the year and beyond.

Metals and Mining

The gold price corrected as of Friday, the 8th of January, closing below $1,900 per ounce after gaining for three consecutive weeks. The fall was caused by the strengthening of the US dollar and the 10-year Treasury yield. Ahead of the break-in at the Capitol building last Wednesday, gold reached a five-day peak of US$1,956; it was valued at $1,863.88 as of 11.01 a.m. EST on Friday. Downward pressure was also felt from the rising bitcoin value that set a record all-time high of US$41,000. Demand for bitcoin rose 39% from the 1st of January, causing a 2% decline in the price of gold. The corresponding movements in prices of these two investment vehicles appear to suggest that the market perceives them as competitors.

Silver likewise ended the week down after mid-week volatility. Values climbed to a five-day high of US$27.79 per ounce before the open of trading on Wednesday, the January 6th; a sharp decline followed thereafter. The downward momentum continued on Thursday, dipping below US$26 to settle at US$25.81 on Friday. Platinum rose to a 10-month high at $2,394 per ounce on Tuesday then corrected to a low of $2,226 then rebounded to end the week at US$2,247.

While the broad precious metals sector may experience further volatility, base metals were buoyed by a positive outlook over potential infrastructure development. Copper, zinc, nickel, and lead prices all made strong showings for the week due to strong forecasted demand.

Energy and Oil

The commitment by Saudi Arabia to further reduce production has fueled a solid rally that saw Brent topping $55 per barrel before the week’s close. Other developments were at play, such as the monetary stimulus package, potential for a deeper stimulus moving forward, and optimism on the effectiveness of the covid vaccine. The steady rise over the last two and a half months, with one slight interim correction, suggests an underlying market resiliency that is expected to remain bullish in the medium term. In the US., the near-term future of shale is bleak as the likelihood of an increase in supply will remain lackluster for the coming years. Aggressive drilling has been dismissed by shale producers as they project annual growth to remain capped at 5%.

In related developments, coal prices are rising as China’s demand for heat increases due to the prevailing cold winter in the northern hemisphere. Producers of lithium, which makes renewable energy possible, saw a severe drop in prices in anticipation of rising production costs, but there remain strong incentives to be bullish about this energy-linked sector. One reason is the full swing of automotive manufacturing from fossil fuels to renewable energy. The share price of Tesla, the leading electric vehicle (EV) manufacturer, rose more than 700% over the past year. Other stocks in the EV sector have shown similar gains.

Natural Gas

U.S. exports of liquefied natural gas (LNG) achieved a record high in the last month of 2020, continuing its November trend with an average of 9,8 billion cubic feet per day (Bcf/d). JKM benchmark prices for LNG continues to soar as spot prices for delivery in kay Asian LNG-consuming countries surged to a six-year high in large part due to the prevailing colder-than-normal winter. This compensates for the historically low prices encountered from April to July 2020 in Asia and Europe. The price slump began to reverse in August, and prices have now more than quadrupled. Since mid-October, prices for natural gas and LNG in the global spot and futures markets have exceeded the crude-oil indexed long-term LNG contracts despite the latter’s increase since September. The recent price increase in long-term contracts resulted from supply shortages caused by unplanned outages of several global export facilities. Fifty percent of U.S. exports since June went to Asian countries, 30% to Europe, and the remainder to the Middle East, Africa, and Latin America, according to reports by the U.S. Department of Energy and the U.S. Energy Information Administration (EIA) as of November 2020.

World Markets

Stricter lockdowns in Europe imposed in response to coronavirus resurgence have generally been shrugged off by the markets. Prices rose on hopes of renewed recovery resulting from a swift vaccine distribution and a potential massive U.S. stimulus package. The pan-European STOXX Europe 600 Index closed the week 3.04% higher. Gains were registered by Germany’s Xetra DAX Index (2.41%), Italy’s FTSE MIB (2.52%), and France’s CAC 40 (2.80%). UK’s banking and energy sectors led the 6.39% surge in the FTSE100 Index. Core eurozone government bond yields likewise ended higher, despite being tempered by weaker-than-expected eurozone inflation data and continued pandemic concerns. Peripheral eurozone bond yields fell for the week as it responded inversely to the core markets. Demand for high-quality government bonds fell while UK gilt yields rose. Germany’s economic data remained strong with better-than-expected trade and production figures together with robust factory orders data, suggesting a fourth-quarter expansion.

In Asia, Japan’s Nikkei 225 Stock Average advanced 2.5% to close the week at a multi-decade closing high of 28,139.03. The yen weakened against the U.S. dollar to close near JPY 104. A new spike in coronavirus cases has prompted Prime Minister Yoshihide Suga to declare a state of emergency in Tokyo and its surrounding prefectures effective Friday, January 9th. Measures to be implemented by the prime minister will be “limited and concentrated” to minimize the adverse economic impact. In China, the CSI 300 Index gained 5.5% and the Shanghai Composite Index rose 2.8% over their December 31 closing levels. Investor sentiment was shaken, however, over NYSE’s delisting of three Chinese telecommunication companies.

In other key markets, Saudi Arabia’s Tadawul All Share Index experienced a 5% correction from its strong close on December 31st. Earlier in the week, investors were greeted with the positive news of the resumption of normal trade and travel ties between Qatar and Saudi Arabia, the UAE, Bahrain, and Egypt. On January 5th, the five nations signed the reconciliation agreement that ended the three-and-a-half-year rift between them. On the same day, OPEC and non-OPEC oil-producing nations (aka Opec+) agreed to keep production flat. In Mexico, the IPC Index declined by 6% over the week. Inflation was reported at 3.15% year-over-year compared to 3.33% in November, which was generally in line with expectations.

The Week Ahead

The coming week signals the unofficial start to the earnings season during which time quarterly earnings reports are expected to be issued by national and regional banks. Important economic data to be released include industrial production, retail sales, and inflation figures.

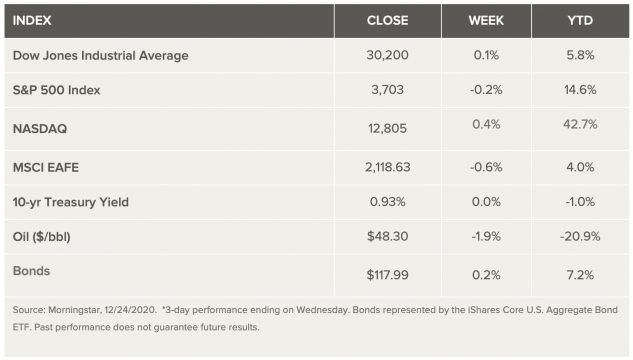

Stocks were mixed last week as investors weighed lawmakers’ approval of a long-awaited relief bill against ongoing virus concerns and new U.K. travel bans. Small cap and technology stocks were up, with both the Russell 2000 and Nasdaq indexes finishing the week higher. The U.S. has continued its vaccination effort, with over 1 million people receiving the first dose of the new vaccine. The president has cast doubt over the passage of the new relief bill, but analysts think it is likely to pass because it contains key funding for vaccine distribution. Consumer confidence has seen a short-term dip, and weekly jobless claims rose unexpectedly, pointing to continued strain from economic restrictions across the country.

US Economy

The year 2020 will go down in history as one of the most memorable and unpredictable years of our lives. The pandemic and resulting health crisis upended everyone, creating unique challenges for individuals, businesses and governments. From a financial-markets perspective, 2020 was a year of unprecedented change but eventual resiliency. As governments imposed strict lockdowns to buy time for the health care systems that were threatened to be overwhelmed, the economy plunged into a deep self-induced recession. However, swift and aggressive policy support helped prevent this health crisis from evolving into a prolonged, full-blown financial crisis. With a week left to go in the year, the light at end of the tunnel is brighter as a result of the medical breakthroughs around vaccine development. Major market indexes are trading near record highs, reflecting a positive 2021 outlook, an outcome that was hard to envision during the early days of the pandemic.

Energy and Oil

Crude oil prices moved higher as the week ended after the Energy Information Administration reported an inventory draw of 600,000 barrels for the week to December 18. This compared with a draw of 3.1 million barrels estimated for the previous week and an inventory build of 2.7 million barrels for the week to December 18, as estimated by the American Petroleum Institute and reported Thursday. Analysts had expected the EIA to report an inventory draw of 3.25 million barrels for last week. Oil prices have been on the rise the past two weeks on positive vaccine news and hopes for a rebound in demand once vaccinations started on a large scale. However, earlier this week, oil reversed its climb on the news about a new, more virulent variant of the coronavirus infecting thousands in the UK and prompting new travel restrictions in Europe and other parts of the world. The news saw oil traders exit their positions in droves, driving prices down. A decline in crude oil buying by Asian refiners also contributed to the most recent reversal of oil prices’ fortunes. Meanwhile, the EIA reported an inventory decline in gasoline, to the tune of 1.1 million barrels, with production last week averaging 8.8 million bpd. This compared with an inventory build of 1 million for the week before last and average production of 8.5 million bpd. Natural gas spot prices rose at most locations this week. The Henry Hub spot price rose from $2.45 per million British thermal units (MMBtu) last week to $2.67/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the January 2021 contract increased 24¢, from $2.442/MMBtu last week to $2.677/MMBtu this week. The price of the 12-month strip averaging January 2021 through December 2021 futures contracts climbed 20¢/MMBtu to $2.780/MMBtu.

World Markets

Shares in Europe were roughly flat for the week ended Thursday, as hopes for a UK-European Union (EU) trade deal helped reverse sharp losses caused by the emergence of a new variant of the coronavirus.

The UK and the EU finally agreed on a post-Brexit trade deal, with the announcement coming after UK markets closed. The accord still must be approved by all EU member states. The agreement’s terms would represent a significant change in the relationship with the UK’s major trading partner and, some say, amounts to a “hard” Brexit in all but name. The Office for Budget Responsibility has forecast that Brexit will cost the UK 4% of its gross domestic product (GDP) over 15 years.

The EU approved the Pfizer-BioNTech vaccine for COVID-19, the disease caused by the coronavirus. The companies said they would supply 12.5 million doses to the EU by the end of the year, Reuters reported. The EU Commission also doubled its orders for Moderna’s vaccine to 160 million doses, with delivery expected to start in early 2021.

China’s benchmark stock index fell for the week ended Thursday as a flareup in Sino-U.S. tensions weighed on sentiment. The Shanghai Stock Exchange (SSE) Composite Index shed 1.0% over the four days ended Thursday, while the large-cap CSI 300 Index was nearly flat. On Monday, the Trump administration published a list of Chinese and Russian companies that it alleged had ties to their countries’ militaries. The list of 58 Chinese and 45 Russian companies requires a license for anyone seeking to sell them items that could be used for military purposes, according to a Commerce Department statement. The SSE Index recorded its biggest one-day percentage drop since September after the list was published, which marked the latest instance of U.S. actions targeting Chinese companies as President Trump prepares to leave office.

In corporate news, Alibaba Group made headlines after China’s top antitrust regulator announced Thursday that it started an investigation into the e-commerce giant. Separately, Chinese regulators said that they have summoned Ant Group, the world’s largest financial technology company and Alibaba affiliate, to a high-level meeting regarding financial regulations. The coordinated actions show that Beijing is ramping up efforts to rein in the domestic tech companies that it sees as a threat to political and economic stability as the companies have grown larger and more powerful in just a few years.

The Week Ahead

Important economic data being released next week include pending home sales and the Chicago PMI.

Stocks edged higher last week, with all major U.S. indexes hitting fresh all-time highs. Fiscal-stimulus optimism, along with a brighter longer-term outlook driven by the rollout of vaccines, continues to support sentiment. Long-term Treasury yields rose modestly, and oil logged its seventh straight weekly gain. Economic data were mixed, revealing that the economic recovery is losing some momentum amidst rising virus cases and renewed restrictions in activity. The weakness in retail sales and the recent slowdown in job growth sharpened the market’s focus on fiscal aid. Congress appears to be closing in on an agreement on a relief bill worth $900 billion. Analysts think that the proposed fiscal deal will provide the relief needed to support the economy as it makes its way to the other side of the pandemic. They say fundamentals are supportive of the longer-term outlook, but investors should anticipate bumps along the way given some of the near-term headwinds to the economy.

US Economy

Stocks breached record highs again last week, trading within a fairly narrow range that reflected a mix of encouraging and disappointing factors, as well as the typical transition toward year-end holiday market conditions. After a dramatic swing this year from a deep recession and bear-market decline to a budding economic recovery and sharp stock-market rally, the present environment is significantly more balanced1. Last week brought a swath of new information that is consistent with analysts’ view of increasingly challenging current conditions countered by an increasingly positive outlook for next year and beyond. Here’s the updated view based on what happened last week:

The pace of the economic recovery is stalling out as surging virus cases have incited renewed restrictions and lockdowns. Analysts don’t anticipate a return to deep recessionary conditions, but they think the economy will endure a soft patch in early 2021 before finding its footing as the vaccine is widely distributed, ushering in a more vibrant rebound in the second half of the year.

Metals and Mining

After starting the week at US$1,832 an ounce, the gold price rallied strongly, climbing as high as US$1,893.20 by Thursday. An uptick in value for the US dollar weighed the yellow metal down on Friday, pulling it further away from the US$1,900 threshold. The rest of the precious metals also climbed higher over the five-day period; however, palladium was unable to sustain the US$2,200 per ounce level, slipping below the mark twice before rising back. Following a month of declines, gold reached a 30 day high this session. But some of its momentum was lost late in the week as the US greenback pulled away from its year-to-date low. Gold trended lower throughout November as optimism around vaccines increased. Some of that thinking was reversed this week as positive cases of COVID-19 increased rapidly around the globe. Gold was priced at US$1,887.15 on Friday. The silver price also spent the majority of the week climbing higher, holding above US$23 per ounce. Year-to-date, the white metal has added 43 percent to its value. Silver’s ability to rise amid market chaos was recently highlighted by US Global Investors’ Ralph Aldis. Silver was trading for US$25.77 on Friday. Platinum rose to a year-to-date high this week, breaching the US$1,040 per ounce level. The price for the precious metal has been edging higher since mid-November. As mentioned, palladium experienced volatility throughout the session. Pushed as high as US$2,243 on Tuesday, it fell as low as US$2,166 on Wednesday. By week’s end, the autocatalyst metal had regained some lost ground to hold above US$2,200. Friday morning saw platinum selling for US$1,032, and palladium was sitting at US$2,224.

Economic recovery hopes continued to propel copper higher this week. The red metal surpassed its previous year-to-date high to rally to US$7,893 per tonne late in the period. Analysts remain optimistic that the base metal will benefit from the widespread vaccine rollout. Copper was holding in the US$7,900 range on Friday morning. Zinc also hit a year-to-date high this week. Since dipping to a low of US$1,773.50 per tonne in March, the zinc price has surged back 60 percent. As of Friday morning, zinc was valued at US$2,841.50. The rally continued for nickel as well, and it pushed to a year-to-date high on Monday of US$17,594 per tonne. The metal pulled back a day later but was able to end the week holding at US$17,520 on Friday. Unlike the other base metals, lead faced price pressure this week. Values hit a five day high on Wednesday of US$2,062 per tonne and have since pulled back. Lead was valued at US$2,046 on Friday.

Energy and Oil

Crude oil prices held their gains this week and pushed to new highs. In midday trading on Friday, Brent was over $52. Optimism on vaccinations is outpacing the bearish winds from record Covid-19 infections in the United States. Analysts differ on what happens next, but some say oil has more room on the upside. Having been savaged for much of 2020, stocks for North American oil and gas producers have surged in recent weeks. The Canadian Energy Sector Index is up 40% since November 9, and U.S. energy stocks are having their best quarter since 1989. LNG prices have in fact, skyrocket of late. JKM prices shot up over $12/MMBtu in recent days. Energy Intel says a combination of factors is leading to the 80% rally in just three weeks. Supply disruptions in Australia, Qatar and Norway, weather-related supply issues in the U.S., congestion at the Panama Canal, colder temperatures in the Northern Hemisphere. At the same time, Saudi Arabia cut its 2021 budget by 7%, as it seeks to minimize the damage from falling oil revenues. In a different light, after decades of stagnation and multiple false dawns, the hydrogen economy appears primed for a major takeoff. Industry experts are predicting that hydrogen could become a globally traded energy source, just like oil and gas, while the Bank of America says the industry is at a tipping point and set to explode into an $11 trillion marketplace. Natural gas spot prices rose at most locations this week. The Henry Hub spot price rose from $2.45 per million British thermal units (MMBtu) last week to $2.67/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the January 2021 contract increased 24¢, from $2.442/MMBtu last week to $2.677/MMBtu this week. The price of the 12-month strip averaging January 2021 through December 2021 futures contracts climbed 20¢/MMBtu to $2.780/MMBtu.

World Markets

Shares in Europe rose on optimism surrounding coronavirus vaccinations, better-than-expected readings from purchasing managers’ indexes in key eurozone economies, and signs of progress in U.S. congressional negotiations for another round of fiscal stimulus. In local currency terms, the pan-European STOXX Europe 600 Index ended the week 1.48% higher, while Germany’s DAX Index rose 3.94%, France’s CAC 40 ticked up 0.37%, and Italy’s FTSE MIB added 1.26%. In London, the FTSE 100 Index ended the week down modestly, as the UK pound strengthened on earlier optimism over a trade accord with the European Union (EU). UK stocks tend to fall when the pound rises because many companies in the index are multinationals that generate significant overseas revenues.

These encouraging developments likewise appeared to reduce investor demand for assets perceived as havens, sending core eurozone bond yields higher and offsetting concerns about tougher coronavirus restrictions and Germany’s plan for hefty debt issuance next year. Peripheral eurozone bond yields ended the week flat. UK sovereign yields generally increased on growing optimism that the UK and EU could reach a trade agreement. However, dovish messaging from the Bank of England (BoE) amid an uncertain economic outlook, as well as growing worries over tighter coronavirus restrictions, somewhat curbed the rise in gilt yields.

Chinese stocks posted a weekly gain despite recording mild losses on Friday, when the U.S. announced that it was blacklisting China’s top chipmaker and more than 60 other companies for national security reasons. For the week, the large-cap CSI 300 Index rose 2.3%, while the country’s benchmark Shanghai Stock Exchange Composite Index added 1.4%.

On Friday, the U.S. Commerce Department said that it was adding Semiconductor Manufacturing International Corp. (SMIC) to its so-called Entity List, which deprives targeted companies from accessing U.S. technology ranging from software to circuitry. The addition of SMIC to the export blacklist came after the U.S. found “evidence of activities between SMIC and entities of concern in the Chinese military industrial complex,” according to the Commerce Department’s statement.

The Week Ahead

This week’s trading will be cut short by the Christmas holiday on Friday, and markets will close early on Thursday. Data being released include personal income and consumption, consumer sentiment, and new home sales.

Key Topics to Watch

Chicago Fed national activity index

Gross domestic product revision (SAAR)

Consumer confidence index

Existing home sales (SAAR)

Personal income

Consumer spending

Core inflation

New home sales (SAAR)

Consumer sentiment index

Initial jobless claims (regular state program, SA)

Stocks edged higher last week as the market’s historic rally extended to the first week of December. Despite a notable slowdown in hiring that was revealed in the November jobs report, major indexes closed at record highs and Treasury yields rose, reflecting expectations for additional fiscal stimulus. The U.S. economy added 245,000 jobs in November, missing estimates amid a spike in COVID-19 infections and renewed restrictions in activity. The unemployment rate declined to 6.7% from 6.9%, but the participation rate also declined, indicating that more people exited the labor force. The silver lining is that the downshift in job gains could apply pressure to lawmakers to reach an agreement for a new stimulus package before the end of the year. Oil extended its gains to a nine-month high after OPEC and its allies agreed to increase production more gradually than previously planned, and the dollar hit a new two-and-a-half-year low against major currencies.

US Economy

Stocks take their direction from economic, earnings and policy fundamentals, not the calendar. That said, December has historically been a positive month for the market, with an average monthly gain of 1.6%. When the stock market enters December on a positive note, that momentum has often been carried through the remainder of the year. Over the past 75 years, when stocks have started the final month of the year with a year-to-date gain of 10% or more (as is the case this year), the market posted a positive gain for December 82% of the time. And the market rose by an average of 7.8% over the following year.

Stocks have now recouped the bear-market losses from earlier this year, reaching a new record last week. With equities up more than 60% since late-March, this has been the fastest recovery from a 30%-plus market drop on record. Markets don’t travel in a straight line indefinitely, and while analysts think 2021 will be a positive year for the markets, they expect the path ahead to be bumpier than the one we’ve traveled over the past eight months. The good news: Recovering the losses from a bear market didn’t mark an exhaustion point for stocks. Looking back at the bear markets since WWII, once the market returned to the previous high, the market gained an average of 14.3% over the following year.

Metals and Mining

After four weeks of declines, the gold price strengthened this week amid speculation that the US may pass a US$908 billion stimulus package before the new year. Gold steadily retreated in November after positive news in the pharmaceutical sector regarding COVID-19 vaccines. The yellow metal’s climb coincides with a dramatic decrease in the value of the greenback. The US Dollar Index slipped to its lowest point in two and half years this week, falling below 90.6. Gold entered the first week of December trading at US$1,773 per ounce and had moved 3.4 Although Q4 has brought added headwinds for gold, there are catalysts pointing to higher prices in 2021. Central banks have also begun purchasing gold again after becoming net sellers in August and September. “(Year-to-date) central bank net purchases continue to sit between 200-300 tonnes,” reads a report from the World Gold Council. Gold was trading for US$1,833.43 on Friday. The silver price started December with momentum, surging 8 percent between Monday and Tuesday. Adding another 1.9 percent to its value, the white metal topped out at US$24.26 per ounce after hours on Thursday. 2020 has been a breakout year for silver, which added as much as 57 percent to its price when it rocketed to US$28.32 in August. Pressure has pushed the white metal back, and it has held above US$22 since. On Friday, silver was moving for US$24.03. After falling to an 18 year low of US$608 per ounce in March, platinum has climbed to a four year high. The automotive metal broke the US$1,070 threshold as markets opened Friday. Since November, platinum has added 24.4 percent to its value, driven higher by production challenges out of South Africa. Most significant are the output constraints that sector leader Anglo American has experienced at its Anglo converter plant. Platinum was selling for US$1,046 on Friday While platinum has steadily trended higher during the first week in December, palladium has experienced volatility. Stable growth in November was upended this week. Hitting US$2,295 per ounce on Tuesday, prices had tumbled 5 percent to US$2,162 by Thursday. The metal has since moved back above US$2,200.

Copper continued its ascent into record territory this week, reaching a fresh seven year high on Friday. The red metal has added 14 percent to its value since early November and is still poised to climb higher. As of Friday morning, copper was priced at US$7,767. Zinc started the session strong, marking a year-to-date high of US$2,809 per tonne. Values fell back as the week progressed, but still maintained record levels. By week’s end, zinc was holding at US$2,747. Nickel prices rose to a one year high in late November, driven higher by positive electric vehicle fundamentals. After climbing to US$16,373 per tonne, prices have slipped back below US$1,600 since the beginning of December. On Friday morning, nickel prices were sitting in the US$15,937 range. In the lead space, prices also faced headwinds this week. A month of growth in November brought prices to US$2,117.50 per tonne, a level unseen since mid-January. However, the higher threshold was unsustainable, and the metal slipped back to US$2,046 at the end of the five-day period.

Energy and Oil

Oil prices rose after OPEC+ agreed to partial increases in production beginning in January, preventing a breakdown in the agreement. Brent inched close to $50 per barrel in a sign of confidence in the deal. It seems that OPEC+ has agreed to monthly increases. Discord characterized the OPEC+ meeting this week, and concerns grew that the group would fail to agree to postponing the planned production increases. But in the end, instead of allowing cuts to ease by 2 mb/d, the group agreed to monthly incremental production increases of just 0.5 mb/d. They also agreed to meet monthly going forward in early 2021 to assess the health of the market. The deal was not as bullish as market analysts had expected, but neither was it a failure. The reaction in oil prices suggests OPEC+ did enough to maintain market stability. Natural gas spot prices rose at most locations this week. The Henry Hub spot price rose from $2.28 per million British thermal units (MMBtu) last week to $2.70/MMBtu this week. At the New York Mercantile Exchange (Nymex), the December 2020 contract expired last week at $2.896/MMBtu. The January 2021 contract price decreased to $2.780/MMBtu, down 18¢/MMBtu from last week to this week. The price of the 12-month strip averaging January 2021 through December 2021 futures contracts declined 8¢/MMBtu to $2.773/MMBtu.

World Markets

Shares in Europe paused after last month’s strong rally. In local currency terms, the pan-European STOXX Europe 600 Index ended the week with a modest 0.21% gain. Major European indexes were mixed: France’s CAC 40 ticked up 0.20%, Germany’s DAX Index fell 0.28%, and Italy’s FTSE MIB slipped 0.78%. The UK’s FTSE 100 Index, however, gained 2.87%, reaching nine-month highs on news that the UK had approved the coronavirus vaccine developed by Pfizer and BioNTech.

Core eurozone bond yields increased overall, lifted early in the week by expectations for further economic stimulus in the U.S. and encouraging developments related to coronavirus vaccines. Core bond yields pulled back somewhat on news that the eurozone purchasing managers’ index (PMI) had declined from the previous month, driven by weakness in the services segment of the economy. Consumer prices in the eurozone declined 0.3% year over year in November, the fourth consecutive month of negative inflation.

Chinese stocks posted their third straight weekly gain, aided by solid economic data. The large-cap CSI 300 Index rose 1.7%, and the benchmark Shanghai Composite Index gained 1.1%, according to Reuters. The yield on China’s 10-year sovereign bond edged lower 3 basis points to end at 3.33%. In currency markets, the renminbi appreciated by 0.5% against the U.S. dollar to CNY 6.5342.

The Week Ahead

Important economic data being released include the small business optimism index on Tuesday, inflation on Thursday, and consumer sentiment on Friday.

This week has seen positive coronavirus-vaccine news, which helped propel the Dow Jones up more than 12% for the month, crossing the 30,000 mark for the first time, and on-track to have the best monthly gain since January 1987. The S&P 500 and Russell 2000 both posted fresh record highs as well. Trading was cut short last week, with Thanksgiving Thursday off and the equity markets closing early on Friday. Economic data releases were light, putting the emphasis on the high-wire act investors are walking between positive vaccine news and rapidly climbing cases and hospitalizations. Analysts think the longer-term outlook remains positive for stocks, but investors should expect spurts of volatility as we turn the page on 2020.

US Economy

“Dow 30,000” has a nice ring to it, but the more important question is: What does this number mean for investors? The underlying factors that have gotten the market to this level are more significant than the number itself. Nevertheless, reaching the 30K mark offers us an opportunity to reflect on the Dow’s milestones: Dow 30,000 is no more significant than 29,928 or 30,169 in the bigger picture. The Dow first crossed the 10,000 level in 1999 to substantial fanfare but proceeded to cross above and below that threshold numerous times in the following years. It last touched 10,000 in 2010. The 25,000 level has been crossed dozens of times since it was first reached in 2018, including as recently as this June. Market index levels can serve as historical measuring sticks, but don’t, in analysts’ view, have particular bearing on the market’s path ahead.

Metals and Mining

The gold price continued to tumble lower this week, dragged down by more positive COVID-19 vaccine news. The optimism around the latest vaccination announcements translated into economic rebound hopes, which weighed on safe haven demand. The yellow metal fell as low as US$1,776.59 per ounce on Friday after dropping 1 percent since Thursday. It hasn’t slipped below US$1,800 since July. Silver also faced headwinds during the last full week of the month, shedding US$2 by week’s end. Speaking about gold’s descent, Peter Grandich of Peter Grandich & Company reminded investors to look at big picture drivers such as continued currency debasement. On Friday, gold was priced at US$1,783.25. Silver’s correlation to gold drove the white metal lower this week as well. Renewed economic optimism wasn’t enough to push silver’s industrial side higher. Starting the period at US$24.05 per ounce, silver trended lower for the rest of the week, bottoming out at US$22.41 when markets opened on Friday. The 6 percent decline was the sharpest decrease silver has experienced since September. On Friday, silver was valued at US$22.70. As gold and silver faced volatility, platinum and palladium were able to edge out small gains. Platinum slipped briefly mid-week but recovered, ending the period slightly higher than Monday. Palladium faced a similar trajectory, shedding value mid-week and then rallying back. By Friday morning, platinum was trading for US$960 per ounce, while palladium was selling for US$2,269 per ounce.

The base metals displayed a mixed performance for the final week of November. Lead pulled off a 2 percent uptick for the best performance of the week. It was followed by copper, which had edged 1.9 percent higher by week’s end. Lead has steadily moved higher since early November, adding 14 percent to its value since the beginning of the month. On Friday morning, lead was priced at US$2,031 per tonne. Copper followed a similar path, save for some volatility experienced mid-month. The red metal has climbed 9.5 percent since November 1, motivated by economic growth in key countries. Prices could be further helped by a 4 percent year-on-year decline in mine supply forecast by Refinitv. By Thursday, copper prices breached US$7,500 per tonne for the first time since 2013. Copper was selling for US$7,511 Friday. Despite issues with mine supply earlier in the month, zinc prices traded sideways this week. Starting the period at US$2,756 per tonne, the metal dipped to US$2,727 on Wednesday. By Thursday, prices had crept higher, holding at US$2,754.50 into Friday. Nickel also benefited from a rally in base metals prices, but that could be short-lived, according to another Fastmarkets report.

Energy and Oil

Oil prices have held on to recent gains despite Covid-19 headwinds. Investors are growing increasingly optimistic and looking beyond the immediate crisis. “It’s a total change of vibe,” Robert Yawger, director of the futures division at Mizuho Securities USA, told the WSJ. “Everything is much more positive now.” OPEC+ is now leaning towards a three-month extension, although not every member is on the same page. Oil prices are holding firm on expectations that the group avoids letting the production cuts ease as scheduled in January, and instead pushes that off until the end of the first quarter at least. The leaders of the OPEC+ pact, Saudi Arabia and Russia, have requested an informal meeting of the Joint Ministerial Monitoring Committee (JMMC) to be held on Saturday, before the alliance’s formal meetings on November 30 and December 1 to decide whether to extend the current level of oil production cuts. Natural gas spot prices fell at most locations this week. The Henry Hub spot price fell from $2.77 per million British thermal units (MMBtu) last week to $2.36/MMBtu this week. At the New York Mercantile Exchange (NYMEX), the price of the December 2020 contract decreased 32¢, from $3.031/MMBtu last week to $2.712/MMBtu this week. The price of the 12-month strip averaging December 2020 through November 2021 futures contracts declined 21¢/MMBtu to $2.779/MMBtu.

World Markets

European shares rose for a fourth consecutive week, fueled by positive vaccine developments, fading U.S. election uncertainties, and expectations that the U.S. Congress may compromise on a smaller economic stimulus. However, the advance lost steam after the UK and Germany extended coronavirus restrictions and vaccine euphoria waned. In local currency terms, the pan-European STOXX Europe 600 Index ended the week 0.93% higher, while Germany’s DAX Index advanced 1.51%, France’s CAC 40 rose 1.86%, and Italy’s FTSE MIB added 2.92%. The UK’s FTSE 100 Index was little changed.

Core eurozone bond yields held firm overall despite a mixed week. Germany’s 10-year bund yield initially rose on more positive vaccine news. However, dovish messaging from the European Central Bank’s Philip Lane ahead of the European Central Bank’s (ECB) policy meeting next week reaffirmed market expectations for more stimulus, dragging yields back down to Monday’s levels. This dovishness pushed peripheral bond yields lower overall, with Portugal’s 10-year yield falling into negative territory. UK gilt yields also fell. Lingering Brexit worries and renewed concerns over economic growth prospects drove the decline, outweighing earlier increases in sentiment supported by vaccination progress.

Chinese stocks rose for the week as solid economic data outweighed concerns about rising defaults among domestic bond issuers. The blue chip CSI 300 Index added 0.8% while the Shanghai Composite Index gained 0.9% for the week, according to Reuters. In fixed income markets, the yield on the sovereign 10-year bond ended the week roughly unchanged. In currency trading, the yuan ended broadly flat against the U.S. dollar. A recent uptick in defaults in China’s high yield bond market has raised expectations that Beijing will focus on corporate sector deleveraging in the near term, as opposed to further stimulating the economy.

The Week Ahead

Economic series being released this week include pending home sales, Manufacturing PMI, and the unemployment rate.

Key Topics to Watch

Chicago PMI

Pending home sales index

Markit manufacturing PMI

ISM manufacturing index

Construction spending

Motor vehicle sales (SAAR)

ADP employment report

Beige Book

Initial jobless claims (regular state program, SA)

Last week saw the equity markets performing a balancing act between incoming positive vaccine news and ever-growing economic restrictions aimed at curbing the recent spike in virus cases and hospitalizations. The rotation out of the technology sector and into more cyclicals stocks continued, as the vaccine developments improved investor sentiment and confidence about next year’s outlook. The jobs-data release showed worse-than-expected initial jobless claims, which, in our view, confirms that this economic recovery is likely to be choppy before ultimately returning to pre-pandemic levels. Reports that the Treasury department is not extending certain funding for the Fed’s lending facilities established earlier in the pandemic is catching attention, though analysts don’t interpret this as a signal that monetary-policy support will be significantly or permanently scaled back.

US Economy

A central theme in equity markets over the last two weeks has been the so-called rotation, or change in leadership across asset classes, sectors and investment styles. We received a series of positive vaccine announcements, first from Pfizer on 11/9, then from Moderna last Monday, and then from Pfizer again last Wednesday on the final results of its late-stage trial. This news propelled the S&P 500 to a new all-time high, before the rally fizzled later in the week on deteriorating coronavirus trends. The near-term outlook is also worsening because of the renewed restrictions on activity. As the market attempts to balance this weakened near-term outlook against an improving medium- to long-term outlook due to the vaccine developments, analysts see this tug-of-war likely continuing between the year-to-date leaders and the economically sensitive investments that have lagged.

Metals and Mining

Gold continued to trade below US$1,900 per ounce this week, held down by positive news on the COVID-19 vaccine front. The yellow metal also faced pressure after the US Department of the Treasury made an announcement about ending emergency loan programs. Facing three months of price pressure, gold was on track for its second week of declines below the key US$1,900 threshold. The rest of the precious metals had better performances during the period, with platinum adding as much as 8 percent to its value this week. As stocks rallied over reports that Moderna is advancing its COVID-19 vaccine, the gold price slumped, dipping to a low of US$1,856.30. Some risk-on sentiment waned when key lending programs in the US were given an expiration date of December 31, 2020, by US Treasury Secretary Steven Mnuchin. Following the announcement, doubts rose around the future of stimulus and fiscal support. Despite the recent trends and vaccine pressure, Independent Speculator Lobo Tiggre sees gold’s fundamentals as more nuanced. At 10:05 a.m. EST on Friday, gold was priced at US$1,877.03. The silver price rose sharply on Friday morning, recovering some early week losses. Starting the session at US$24.53 per ounce, the value of the white metal had slipped 3 percent by Thursday. The metal’s ability to retain its value amid the headwinds gold is experiencing underline positive fundamentals moving forward. The white metal was valued at US$24.41 on Friday. The price of platinum has been edging higher since the morning bell rang on Monday. Adding as much as 8.2 percent, platinum has pulled back slightly but remains above US$950 per ounce. The recent price activity has been propelled by a decrease in platinum output, likely to be compounded by Anglo American Platinum’s closure of the Phase B unit at its convertor plant in South Africa. Platinum was selling for US$951 on Friday. After making steady gains since the beginning of the month, palladium faced volatility this session. The headwinds prevented any gains from locking in and aided in a dip below US$2,200 per ounce. By Friday, the metal was fluctuating just above US$2,200. Palladium is poised to perform well on the back of similar drivers in the platinum market. On Friday, it was moving for US$2,194.

The base metals sector also faced difficulties this week but managed to mitigate losses. Copper started the week trading at US$7,113 a tonne and fell lower over the period. Prices declined 1 percent by Thursday, and copper was selling for US$7,028 on Friday morning. Nickel also faced challenges, dropping 2 percent on Tuesday. Following a small rally on Wednesday, prices slipped to US$15,690 per tonne a day later. Nickel remained at that level on Friday. Two base metals were able to squeak out gains this week: zinc and lead. Starting the period at US$2,653 per tonne, zinc had climbed as high as US$2,732.50 by mid-week. By week’s end, the metal was holding at US$2,721. Lead also edged higher, adding 3.6 percent to its Monday value of US$1,882.50 per tonne. Lead has consistently moved higher since November 11, adding 7.3 percent to its worth. On Friday morning, lead was priced at US$1,951.

Energy and Oil

Oil prices pared recent gains as investors nervously watch the spread of Covid-19, which has tempered bullishness following positive vaccine news. “It’s not good news,” Bill O’Grady, executive vice president at Confluence Investment Management in St. Louis, told Bloomberg. “This is probably going to be a disappointing travel holiday coming up, and that’s going to weigh on demand.” Still, there are signs of life in global oil demand visible beyond the near-term coronavirus wave. Asia’s oil demand continues to look strong. While oil demand in Europe and the United States continues to disappoint, refiners in Asia are racing to procure crude from around the world, giving the oil market some hope that at least in one region, demand is strengthening in the fourth quarter. China’s oil binge to extend into 2021. China stockpiled oil this year when prices were cheap, offering an extra bit of demand to the market. Reuters reports that China’s private refiners will stockpile an additional 100 million barrels in 2021. Oil demand appears primed for recovery as crude oil demand is likely to rebound next year following the promising news about a vaccine against the novel coronavirus, according to Fitch Ratings.

Natural gas spot prices fell at most locations this report week (Wednesday, November 11 to Wednesday, November 18). The Henry Hub spot price fell from $2.77 per million British thermal units (MMBtu) last week to $2.36/MMBtu this week. At the New York Mercantile Exchange (NYMEX), the price of the December 2020 contract decreased 32¢, from $3.031/MMBtu last week to $2.712/MMBtu this week. The price of the 12-month strip averaging December 2020 through November 2021 futures contracts declined 21¢/MMBtu to $2.779/MMBtu.

World Markets

Hungary and Poland blocked the European Union’s (EU) planned EUR 1.8 trillion fiscal package, which includes a large fund to help economies weather the damage caused by the coronavirus. They oppose a mechanism that would allow the EU to block disbursements to countries violating its rule of law principles. The Politico news website reported that EU leaders at their Thursday videoconference summit did not indicate how the standoff might be resolved. German Chancellor Angela Merkel said she would hold talks with the leaders of the two countries while defending the existing proposal.

Reports suggest that three main areas of contention—a level playing field for companies, fishing rights, and settling trade disputes—persist as the UK and EU negotiate a post-Brexit agreement on trade. Face-to-face talks have been suspended because a senior negotiator tested positive for COVID-19, although officials will keep working remotely, according to Reuters. France, the Netherlands, and Belgium urged the European Commission to start implementing contingency measures in case there is no deal before the Brexit transition ends on December 31.

Chinese stocks rose strongly after solid economic data lifted investors’ risk appetite. For the week, the large-cap CSI 300 Index gained 1.78% while the benchmark Shanghai Stock Exchange Composite Index added 2.04%, according to Reuters data. In fixed income markets, the yield on the sovereign 10-year bond increased six basis points to 3.34%. In currency trading, the renminbi strengthened by 0.6% against the U.S. dollar to close at 6.570. The People’s Bank of China (PBOC) injected RMB 800 billion (about USD 121 billion) in medium-term loans into the banking system and left interest rates on hold for the seventh straight month. The central bank also kept its one-year medium-term lending facility rate to financial institutions unchanged at 2.95%.

The Week Ahead

Important data being released this week include personal income and spending breakdowns, FOMC minutes, and building permits.

Key Topics to Watch

Chicago Fed national activity index

Markit manufacturing PMI (preliminary)

Markit services PMI (preliminary)

Case-Shiller national home price index

Consumer confidence index

Initial jobless claims (regular state program, SA)

Initial jobless claims (federal & state, NSA)

Continuing jobless claims (regular state program, SA)

Following three consecutive weekly advances, stocks declined modestly last week. The news flow was dominated by headlines around the negotiations for another round of fiscal relief from Washington before the election, which is fast approaching. The 10-year Treasury yield rose to the highest level in four months amid expectations that a potential Biden win would lead to a larger relief package to support the economy. Aside from the speculation about potential election outcomes and policies, economic data for the week was encouraging to the long-term outlook, showing an improvement in jobless claims and continued strength in the housing market.

US Economy

Markets behaved in a somewhat orderly fashion last week, oscillating in a fairly narrow band that left U.S. equities slightly in the red for the week. We’d stop short of labeling last week the ‘calm before the storm” because analysts think there are credible reasons for stocks to have a toehold. That said, analysts think investors would be well served to brace for a bumpier ride as we work our way to, and through, the election.

Current conditions are prompting a perception among some investors that the election represents a binary outcome for the market. November 3 may be viewed as a seminal moment in our country’s political landscape, but when it comes to investing, it’s the much broader periods of time – not singular moments – that matter most. In addition to political headlines and reasonably encouraging economic readings, last week brought a few market anniversaries, including the 33rd anniversary of the “Black Monday” crash.

Metals and Mining

After the second and final US presidential debate on Thursday, gold moved above the key US$1,900 per ounce threshold. After slipping below that level earlier in the week, investors regained hope that a US stimulus package could be close at hand. Gold’s steady growth trend was disrupted this week as the US dollar strengthened, adding volatility to the yellow metal’s value. The other precious metals were also on course to end the week in the green. Entering the five-day period at US$1,910 before slipping to US$1,895 on Wednesday, a subsequent rally pushed gold as high as US$1,927 by the headwinds mentioned. Because gold is considered a hedge against inflation and currency debasement, the next round of stimulus is expected to add to its value. On Friday an ounce of gold was trading for US$1,893.66. Silver had been locked at the US$24 per ounce range since the end of September but moved above US$25 briefly this session. While the trend to US$25 was unsustainable, silver remained above US$24.50 for the remainder of the week. The nature of the dual metal as a leveraged play on gold has worked in its favor, prompting analysts to note that during bull markets silver traditionally outperforms gold. That was evident during Q3, when silver outpaced its yellow sister significantly. During the period, silver added 34 percent to its value, gaining more than 60 percent year-to-date at its quarterly peak. On the other hand, gold added only 6.9 percent to its value in total for Q3, and 16 percent when it touched an all-time high of US$2,063. Though gold and silver have spent the last four weeks edging higher, platinum has been steadily slipping lower. However, that trend was reversed this period, with the automotive metal surging past US$900 per ounce late in the week. Adding 5 percent to value for the week, the metal is positioning to benefit from the rally in precious metals. On Friday, platinum was valued at US$907. The palladium price was also propelled higher this week when it breached US$2,300 per ounce. The price action took palladium back to pre-COVID-19 levels seen in March. But after hitting the six-month high, prices were pressured and fell back to US$2,246. Palladium was selling for US$2,260 on Friday.

The broad base metals space was also in the green on Friday, with all metals registering gains. Copper was the leader, surging to a year-to-date high of US$6,953 per tonne on Wednesday. Demand out of Asia has contributed to the red metal’s ascent to a two-year high. Renewed industrial demand and the US stimulus package are forecast to continue working in copper’s favor. Zinc was also on the move this week, adding 2.7 percent to its value. Despite being shy of its year-to-date high, the metal is still in positive territory. Zinc was trading for US$2,540 per tonne to end the week. Nickel marked a year-to-date high this session when it surpassed US$16,064 per tonne, a 14 percent increase from its January values. The metal has been gaining since late September, as demand from the electric vehicle space is projected to increase. By Friday, nickel had shed some of the gains to trade for US$15,707. Lead also enjoyed a price uptick for the third full week of October. Though it remains well off its year-to-date high, the metal is slowly edging higher and is holding above US$1,700 per tonne. Lead ended the week at US$1,792.

Energy and Oil

On Thursday, the U.S. reported more than 70,000 COVID cases for the first time in three months, and the trajectory suggests the U.S. may break new record highs in the coming days. The numbers help explain weak (and weakening) gasoline demand in the U.S., a theme also unfolding in Europe. The pandemic continues to largely cap any potential price rally. Crude remains stuck at $40, where it has traded for the better part of four months. Demand is weak in Europe, the U.S. and Latin America, and remains depressed as the coronavirus continues to spread. But in Asia, gasoline demand is robust, and even jet fuel demand is rebounding strongly. As Javier Blas notes, there is a very big difference between east and west right now, with Asia looking to pre-pandemic demand levels. IN the final presidential debate, Biden and Trump clashed over oil and climate. While the substance and their positions were not new, the topics of oil, fracking and climate change played a large role in the last presidential debate. Trump has largely ignored the climate science and promises to maintain a friendly stance towards oil and gas. Biden played up the job opportunity of renewables and said the U.S. must transition away from fossil fuels. Democrats propose “blue carbon” bill. A proposal from House Democrats would expand offshore wind while barring new offshore oil drilling.

Natural gas spot price movements were mixed this week. The Henry Hub spot price rose from $2.03 per million British thermal units (MMBtu) last week to $2.86/MMBtu to this week. At the New York Mercantile Exchange (Nymex), the price of the November 2020 contract increased 39¢, from $2.636/MMBtu last week to $3.023/MMBtu this week. This increase marks the first time the near-month natural gas futures price has reached $3.00/MMBtu since January 2019. The price of the 12-month strip averaging November 2020 through October 2021 futures contracts climbed 13¢/MMBtu to $3.133/MMBtu.

World Markets

Shares in Europe fell on signs that the economic recovery was stalling amid tighter restrictions to curb surging coronavirus infections. The pan-European STOXX Europe 600 Index ended the week 1.36% lower, and major country indexes also declined: Germany’s DAX Index slipped 2.04%, France’s CAC 40 gave up 0.53%, and Italy’s FTSE MIB dropped 0.54% The UK’s FTSE 100 Index lost 1.00%, in part reflecting strength in the pound after the resumption of talks with the European Union (EU) on post-Brexit trade ties. UK stocks tend to fall when the pound rises because the index includes many multinationals with overseas revenues.

The German 10-year bund yield inched up on hopes that the U.S. government would pursue additional measures to stimulate its economy. Yields on sovereign bonds from peripheral European economies largely followed suit. Italian government debt yields also climbed after the sale of EUR 8 billion 30-year bonds, which received EUR 90 billion in offers. An inaugural issue of EU 10- and 20-year social bonds attracted bids of more than EUR 233 billion, far exceeding the EUR 17 billion on offer. The issue is part of the EU’s EUR 100 billion SURE (Support to mitigate Unemployment Risks in an Emergency) bond program designed to support jobs.

Chinese stocks retreated for the week, with the large-cap CSI 300 Index and benchmark Shanghai Composite Index shedding 1.5% and 1.8%, respectively. The yield on China’s 10-year sovereign bond decreased, slowing a steady advance dating back to July. On the monetary policy front, the People’s Bank of China Governor Yi Gang said that China’s key debt ratios could moderate in the coming months as economic growth picks up. Yi also stated that the central bank would pursue a balanced approach to supporting China’s economy, saying that monetary policy “needs to guard the gates of money supply and properly smooth out fluctuations” in the country’s macro leverage ratio. The renminbi currency continued its strengthening against the U.S. dollar aided by strong inflows into China’s domestic bond market, whose relatively high yields have attracted foreign investors.

The Week Ahead

The third-quarter earnings season is in full swing, with almost 40% of the S&P 500 companies reporting earnings throughout the week. Important economic data being released include consumer confidence on Tuesday, third-quarter GDP growth on Wednesday, and personal income and spending on Friday.

Key Topics to Watch

Chicago Fed national activity index

New home sales (SAAR)

Durable goods orders

Core capital goods orders

Case-Shiller national home price index (year-over-year change)

The equity markets saw volatility return last week, with Thursday seeing declines of 3% and Friday 1%1. Before this last week, the S&P 500 advanced for four straight weeks, with technology stocks leading the index to a new record high. The strength of the stock market, though, seemingly disconnected from current economic fundamentals, has been supported to date by aggressive fiscal and monetary stimulus and stronger-than-expected economic indicators of future growth. The Department of Labor released data last week showing initial jobless claims coming in at 881,000, beating analysts’ estimates. The economy also added 1.4 million jobs in August, with 10.1% growth in productivity. On the trade front, the U.S. deficit reached a 12-year high.

US Economy

We’re two-thirds of the way through 2020, but the year so far has produced more than its fair share of extraordinary statistics. With Labor Day bringing the unofficial end to an unusual summer, here’s some of the year’s unusual figures and where they are now: While market volatility increased sharply this year, it was particularly notable in March, which included a single-day decline of 12% — the second-worst day in the last 50 years – as well as two 9% daily gains (the third- and fourth-best days) a handful of days apart. After bottoming in late March, the stock market has been on a steady path higher, with relatively modest fluctuations along the way, including only 22 daily moves larger than 2% during that time. Last week saw a return of volatility, with the market falling 3% on Thursday, as many of the higher-flying segments of the market, such as tech stocks, sold off following a lengthy winning streak. Analysts don’t see this as the beginning of a new broader direction lower for the market, but instead a more normal breather for a market that has been on quite a run.

Metals and Mining

The bears in gold could only manage one day in keeping prices down as the yellow metal bounced back Friday from a brief selloff across markets forced by the shock collapse of U.S. gross domestic product in the second quarter.

“Gold mania continues and after tentatively clearing the $2000 level, traders are starting to doubt whether a profit-taking pullback is in the cards,” said Ed Moya, analyst at New York-based online trading platform OANDA. Spot gold, a real-time indicator of trades in bullion, last traded up $19.47, or 1%, at $1,976.11. It fell a meagre 0.6% in the previous session, touching a session low of $1,939.69 that remained well above the level it attained when it rewrote for the first time this week record highs from 2011. On New York’s Comex, the August futures contract last traded up $28.90, or 1.5%, at $1,971.20 before expiring and going off the board. On Thursday, August fell just 0.5%. For July, Comex gold ended up 9%, for its biggest monthly gain since February 2015. For the year, gold futures are up 28%. Further, December gold hit a record high of $2,005.40 in Friday’s Asian session, before the start of European and U.S. trading. That also means the new front-month for Comex would likely aim for a higher peak in the new week to sate gold bulls pursuing $2,000-territory.

Moya expounded that “Gold will continue to shine bright as real yields continue to fall deeper into negative territory, virus surges will keep economic recoveries limited, and the stimulus trade will not go away until the labor market bounces strongly back.” Silver, which rallied along with gold through most of July, rose 36% for the year, outperforming not just the yellow metal but the entire commodities complex as well. Silver’s front-month contract on Comex, September, last traded up $1.263, or 5.4%, on Friday at $24.625 per ounce.

Energy and Oil

Oil prices hit a rough patch this week, falling back in concert with broader financial markets. The dollar gained strength, which also pushed down crude. The demand rebound is also sputtering. WTI was driven below $40 for the first time since June. Iraq is looking for an exemption from the OPEC+ deal for the first quarter of 2021, raising fears that the group’s compliance may start to slip. A separate report says that Iraq wants a two-month extension on the extra production cuts that it agreed to implement in August and September. Kuwait’s budget deficit is expected to reach $46 billion this year. But oil revenues collapsed after the 2014-2016 downturn and never recovered. Now the country is grappling with tapping its sovereign wealth fund as the days of huge oil revenues appears to be over. A new report from the European Commission warns that the shortage of critical materials could threaten the EU’s push to become climate neutral by 2050. The EU estimates that it will need up to 18 times more lithium and five times more cobalt in 2030, a figure that rises to 60 times more lithium and 15 times more cobalt by 2050. Natural gas spot price movements were mixed this week. The Henry Hub spot price fell from $2.51 per million British thermal units (MMBtu) last week to $2.19/MMBtu this week. At the New York Mercantile Exchange (Nymex), the September 2020 contract expired this week at $2.579/MMBtu, up 12¢/MMBtu from last week. The October 2020 contract price decreased to $2.486/MMBtu, down 9¢/MMBtu from last week to this week. The price of the 12-month strip averaging October 2020 through September 2021 futures contracts climbed 10¢/MMBtu to $2.973/MMBtu.

World Markets

European shares pulled back in sympathy with the technology-led decline in U.S. equities. However, news of merger talks between Spanish lenders Bankia and CaixaBank helped to curb losses. In local-currency terms, the pan-European STOXX Europe 600 Index ended the week 1.76% lower. Germany’s Xetra DAX Index fell 1.46%, France’s CAC 40 slid 0.76%, Italy’s FTSE MIB declined 2.27%, and the UK’s FTSE 100 Index dropped 2.76%.

An early estimate of eurozone consumer prices showed inflation of -0.2% in August—the first decline since May 2016—heaping more pressure on the European Central Bank (ECB) to increase stimulus. Speculation that the ECB would have to act soon to counter a stronger euro had mounted before the release of the latest data on consumer prices. The euro’s strength is worrying policymakers, who warned that further appreciation would weigh on exports, drag down prices, and hold back the economic recovery, according to the Financial Times newspaper. Evidence of this unease emerged earlier when the euro briefly rallied to more than USD 1.20 for the first time since 2018, prompting ECB Chief Economist Philip Lane to say the euro-dollar rate “does matter” for monetary policy. The consensus calls for the ECB to keep its policy settings unchanged at its meeting next week.

Mainland Chinese stock markets fell, with both the large-cap CSI 300 and benchmark Shanghai Composite Index shedding 1.5% following the overnight sell-off on Wall Street. The yield on China’s 10-year bond increased and ended the week at 3.14%.

The People’s Bank of China (PBOC) and the State Administration of Foreign Exchange (SAFE) announced simpler rules to facilitate trading of domestic bonds by overseas investors. Under the new measures, foreign investors can access onshore foreign exchange and rate-hedging tools and invest in exchange-traded bond products. Separately, the PBOC said on August 31 that the depositary institutions repo rate (DR) would now be the key short-term reference rate. Following the move, DR rates will become the pricing basis for most money and liquidity products. Along with the medium-term lending facility rate, the new key rate will form the backbone of China’s policy rate system and brings the country a step closer to the rate-setting systems of other major central banks.

The Week Ahead

Important economic releases this week include Consumer Credit, CPI data, and hourly earnings growth.

Key Topics to Watch

NFIB small-business index

Consumer credit

Job openings

Initial jobless claims (regular state program, SA)

Markets finished higher last week, on track for its best August in 34 years, and continuing the rally after the third bear market in two decades. The S&P 500 is up nearly 52% since the bear market bottom on March 23, and is up nearly 8% for the year, posting a new record high of 3,4941. The chairman of the Federal Reserve Board, Jerome Powell, stated last week that the Fed will let inflation run slightly higher than the traditional 2%, meaning rates will stay lower for longer, which is a tailwind for equities. Personal spending rose 1.9% in July, the third month in a row showing growth, indicating that the economic recovery is underway.

US Economy

The health, social and economic effects of COVID-19 continue to be felt, but that hasn’t stopped stocks from marching higher. The S&P 500 closed at another record high last week and is on track to log its best summer performance (June – August) since 1938 and its best August since 1981. The market is wrapping up the summer in a much different position than it was in just a hand full of months ago, reflecting this year’s evolving (and unusual) conditions.

The last three months provided additional evidence that the economy is gradually exiting a deep recession, with data hinting to a sizable bounce in the third quarter. A real-time forecast from the Federal Reserve Bank of Atlanta estimates that third-quarter GDP will grow 26% following a 32% annualized decline in the second quarter. If this proves to be the case, by the end of September the economy will have recovered half of its pandemic-induced losses, leaving real GDP about 5% below its pre-crisis level. Still a lot of ground to cover, but a good first step.

Metals and Mining

After two weeks of losses, gold was poised to end the last week of August up almost 2 percent, reversing a brief slump that saw the metal dip to US$1,917 per ounce on Wednesday (August 26). The yellow metal strengthened as the US dollar pulled back on news that the Fed is taking a dovish stance that is expected to prolong the current low interest rate environment. The other metals were a mixed bag, with silver on track for second week of gains, benefiting from its dual nature as a precious and industrial metal. In a much-anticipated Thursday address, US Federal Reserve Chair Jerome Powell said the central bank will try to achieve an average inflation level of 2 percent over time, meaning it may be higher or lower than that amount at times. In the hours following, gold rose from US$1,917 an ounce to a five-day high of US$1,966.70. He went on to say his firm expects the currency metal to again test the US$2,000 range, possibly moving as high US$2,300. Silver has been trending higher since pulling back in mid-August. The white metal has now added 10 percent to its value since August 11 and is working towards the US$30 per ounce threshold. Even though silver remains shy of its year-to-date high of US$29.14, achieved on August 10, the present price environment is very supportive of pure-play miners, which according to Metals Focus need a price point of at least US$19 an ounce to be economical. Up 53 percent from January, and more than 100 percent since the March slump, silver is expected to show improved resilience as industrial demand strengthens. Platinum lost some ground mid-week, hitting a monthly low of US$905 per ounce. Early in August, the metal had been approaching US$1,000 territory, but retreated. Despite the recent price pressure, analysts are anticipating a rally later in the year. A release from the World Platinum Investment Council touts increased end-use applications for the metal, with the most prominent being an uptick in use as a coating to prevent corrosion or to boost electroconductivity and heat resistance Palladium faced volatility this session, but still held above US$2,000 an ounce. After steadily moving higher in July, the autocatalyst metal has faced headwinds, shedding 7.1 percent month-over-month. Although prices have slumped in August, the metal is well above its January value of US$1,967 per ounce. Palladium was valued at US$2,601 at 12:10 p.m. EDT on Friday.

The base metals managed to squeak out a gain, with the exception of lead. Climbing as high as US$1,984 per tonne mid-week, subsequent pressures weighed the lead price down. Copper posted a strong gain, starting the session at US$6,579.50 per tonne; it pulled back slightly to end the week at US6,602. The red metal is also benefiting from the Fed’s policy shift and renewed optimism that COVID-19 lockdowns will lead to a smaller demand decline that expected. According to an S&P Global report, copper consumption is now expected to fall by 3 to 4 percent year-on-year, less than a 4.6 percent decline in global GDP. Chinese demand, which accounts for half of the metals market, has been robust and will likely prop the market up in the months ahead. Copper was priced at US$6,602 Friday. Zinc felt resistance this week, pulling the metal off its five-day high US$2,462 per tonne. Prices then settled in the US$2,450 range. Zinc has added 38 percent to its value since January, and Friday saw prices sitting at US$2,455. Nickel hit its year-to-date high this week when it rallied from US$14,862 per tonne to US$1,5120. The surge marks the metal’s best showing since November. Since falling to a low of US$11,055 in mid-March, nickel has climbed 36.7 percent. As of Friday, nickel was valued at US$15,120.

Energy and Oil

Oil prices retreated in the wake of Hurricane Laura, which led to much less destruction than the market had anticipated. That leaves the oil price dynamic little changed from the past two months – WTI and Brent are stuck in familiar territory between $42 and $45. The concentration of energy assets along the Texas and Louisiana coast more or less avoided the worst-case scenario from Hurricane Laura. “The damage is not as bad as anticipated, which is creating more sell pressure along the energy complex,” said Phil Flynn, senior market analyst at Price Futures Group. More than 80 percent of oil output in the Gulf of Mexico and almost 3 million barrels a day of refining capacity had been shut ahead of the storm, most of which should come back online fairly quickly. Laura shut-in some LNG operations, and gas exports are set to fall to about 2.1 bcf, the lowest level since February 2019. Oil exports are expected to drop by nearly 1 mb/d this week. Natural gas spot prices rose at most locations this week. The Henry Hub spot price rose from $2.36 per million British thermal units (MMBtu) last week to $2.51/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the September 2020 contract increased 3¢, from $2.426/MMBtu last week to $2.461/MMBtu this week. The price of the 12-month strip averaging September 2020 through August 2021 futures contracts declined 1¢/MMBtu to $2.851/MMBtu.

World Markets

European shares rose on further economic stimulus in France and Germany, a recommitment by the U.S. and China to their partial trade deal, and signs of progress in the development of treatments for COVID-19. In local currency terms, the pan-European STOXX Europe 600 Index ended the week 1.02% higher, while Germany’s Xetra DAX Index climbed 2.10%, France’s CAC 40 added 2.18%, and Italy’s FTSE MIB rose 0.74%. The UK’s FTSE 100 Index slipped 0.6%.

Despite renewed surges in coronavirus infections, France, Spain, and Italy appeared to reject the need for nationwide lockdowns to curb what could be a second wave of the pandemic. French Prime Minister Jean Castex said the government would do everything to prevent a nationwide lockdown but warned that some regions might need to be isolated after cases quadrupled over the past month. In Italy, Health Minister Roberto Speranza asserted that the government was optimistic about keeping the situation under control, noting that there were fewer hospitalizations and fatalities. In Spain, Prime Minister Pedro Sanchez appeared to rule out a countrywide lockdown, saying the current outbreak was far from the situation in March and that officials were better prepared and had a better understanding of the virus.

Mainland Chinese stock markets rose for the week. The blue-chip CSI 300 Index gained 2.7% and the benchmark Shanghai Composite Index, which gives a significantly larger weighting to state-owned enterprises, added 0.7%. For the year to date, Chinese yuan-denominated A shares have gained about 10% compared with a roughly 8.5% gain for the S&P 500 Index, making them among the best performers in global stock markets.

The yield on China’s sovereign 10-year bond increased for the week amid further evidence of the strengthening economy. Industrial profits in July surged 19.6% over a year earlier in their fastest year-over-year growth since June 2018. However, cumulative profits for the year to date remain in negative territory. Profits at state-owned enterprises significantly lagged those at private and foreign-owned companies.

The Week Ahead

Important economic data being released this week include Construction Spending, Continuing Jobless Claims, and the PMI Composite.